Superannuation Retirement Calculator

Calculate your super future

Estimate your retirement savings based on your current situation

Let’s cut through the noise. If you’re asking whether pension plans are worth it, you’re not just curious-you’re probably wondering if your money is being wasted. You’re not alone. Millions of Australians contribute to superannuation every pay cycle, but many still feel unsure if it’s really helping them. The truth? For most people, yes-it’s one of the best financial moves they’ll ever make. But it’s not magic. It doesn’t work if you ignore it, underfund it, or assume it’ll cover everything. Let’s break down exactly what you’re getting, what’s changing in 2026, and whether your pension plan is actually working for you.

What exactly is a pension plan in Australia?

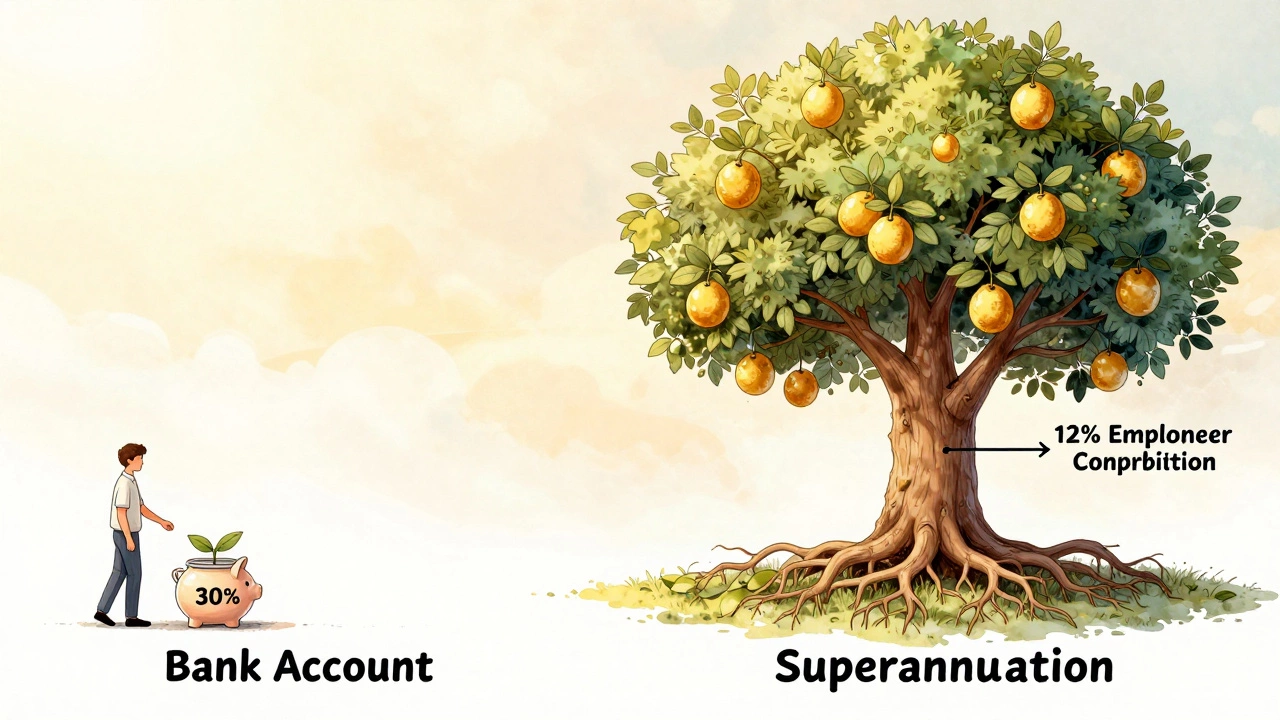

In Australia, the term "pension plan" usually means superannuation is a government-mandated retirement savings system where employers contribute a portion of your salary into a fund you can’t touch until you retire. It’s not optional. Since 2025, the minimum employer contribution rate is 12%, up from 11.5% in 2024. That means if you earn $70,000 a year, your employer is putting $8,400 into your super each year-on top of your salary.

You can also add your own money. Many people contribute extra through salary sacrifice or personal contributions. The government even gives you a tax break if you do. For the 2025-26 financial year, you can contribute up to $30,000 in concessional (pre-tax) contributions without penalty. If you’re over 50 and still working, you might qualify for catch-up contributions if you haven’t maxed out in previous years.

This isn’t just a savings account. It’s a long-term investment vehicle. Your super fund invests your money in shares, property, bonds, and infrastructure. The average super fund returned 7.8% annually over the last decade. That’s after fees and taxes. Some funds did better. Some did worse. But the system as a whole has consistently outperformed inflation.

Why most Australians benefit-big time

Let’s look at a real example. Sarah, 32, works as a teacher in Sydney. She earns $68,000 a year. Her employer contributes $8,160 annually. She adds $200 a month from her paycheck-that’s $2,400 more. Total contributions: $10,560 per year. She’s in a growth fund with an average 7.5% annual return. By age 67, assuming no changes in her income or contributions, she’ll have about $1.2 million in her super.

Now, what if she didn’t do this? If she just saved $200 a month in a regular savings account earning 2% interest, she’d have roughly $270,000 at 67. That’s less than a quarter of what super gives her. And that’s before considering tax advantages.

Super is taxed at just 15% on contributions and earnings-far lower than the marginal tax rate most working Australians pay (32.5% or higher). When you withdraw after 60, it’s tax-free. That’s a massive boost. A $10,000 contribution today could grow to over $80,000 by retirement, thanks to compounding and tax efficiency.

The hidden downsides-what nobody tells you

But here’s the catch: super isn’t perfect. It’s locked away. You can’t access it until you hit your preservation age (60 for most people born after 1964). That’s great for discipline-but bad if you face a financial emergency. Unlike a savings account, you can’t dip into super for medical bills, home repairs, or a job loss.

Also, not all funds are equal. The average fee across Australian super funds is 1.2% per year. But some low-cost funds charge as little as 0.4%. That difference matters. On $1 million, 1.2% means $12,000 in fees annually. At 0.4%, it’s $4,000. Over 20 years, that’s a $160,000 gap. Choosing the right fund isn’t optional-it’s critical.

And then there’s the gender gap. Women, on average, have 30% less super than men at retirement. Why? Career breaks for caregiving, part-time work, and wage inequality. The system doesn’t account for this. If you’re a woman, you need to be extra intentional about topping up your super during career pauses.

How much do you actually need to retire?

Retirement isn’t one-size-fits-all. The Association of Superannuation Funds of Australia (ASFA) estimates that a comfortable retirement for a couple requires about $72,000 per year. For a single person, it’s $51,000. That includes travel, dining out, hobbies, and occasional medical costs.

But here’s what most people don’t realize: those numbers assume you own your home outright. If you still have a mortgage at 65, you’ll need significantly more. And if you want to travel overseas regularly or help your kids with a home deposit, you’ll need even more.

So how much super do you need? A simple rule: aim for 15 times your annual retirement spending. If you want $60,000 a year, you need $900,000. That sounds high-but remember, super grows slowly at first, then explodes later. The magic happens in the last 15 years. That’s why starting early matters more than how much you earn.

What’s changing in 2026?

This year, two big changes are rolling out:

- Superannuation guarantee increases to 12%-this is now locked in. No more gradual hikes. Employers must pay it. If they don’t, you can report them to the ATO.

- MySuper default funds now include ESG filters-if you haven’t chosen a fund, your money goes into a default MySuper account that avoids fossil fuels and tobacco companies. You can opt out, but most people don’t.

Also, the government has expanded the Low-Income Super Tax Offset (LISTO). If you earn under $45,000, you now get up to $500 back in super contributions from the government-even if you didn’t pay tax. That’s free money. If you’re on a part-time wage, casual work, or stay-at-home parenting, this is a lifeline.

Who shouldn’t rely on super?

Not everyone benefits equally. Here are the exceptions:

- High-income earners with no employer-if you’re a contractor who doesn’t get super paid for you, you need to be proactive. Don’t wait. Set up regular contributions.

- People with serious health issues-if you expect to pass away before 60, super isn’t the right tool. Consider life insurance or trusts instead.

- Those with massive debt-if you’re paying 20% interest on credit cards, paying that off first gives you a better return than super.

For everyone else? Super is still the best game in town. It’s automatic, tax-advantaged, and designed for long-term growth. You don’t need to be a financial expert. You just need to be consistent.

What to do right now

Don’t wait for "someday." Here’s what to do in the next 30 days:

- Check your super balance-log into your fund’s website. If you have more than one account, consolidate them. Multiple accounts mean multiple fees eating into your balance.

- Review your investment option-are you still in "growth"? Or did you pick "balanced" years ago? If you’re under 40, growth is still the right choice.

- Calculate your gap-use the ATO’s retirement estimator. It’ll tell you if you’re on track. If you’re behind, increase your contributions by $50 a week. That’s less than a daily coffee.

- Set up a direct debit-even $25 a week from your bank account into super adds up. Over 30 years, that’s over $100,000 extra.

Super isn’t a lottery. It’s a system built on time, consistency, and compound growth. The people who win aren’t the ones who invest the most-they’re the ones who start the earliest and never stop.

Is superannuation really better than saving in a regular bank account?

Yes, for almost everyone. Super offers three big advantages: tax breaks (only 15% tax on contributions and earnings), employer contributions (free money), and compound growth over decades. A regular savings account might earn 2-3% interest, but you pay tax on that interest every year. Super compounds that growth tax-free. Over 30 years, the difference can be hundreds of thousands of dollars.

Can I access my super before I retire?

Generally, no. You can’t touch it until you reach your preservation age (60 for most people) and retire. There are limited exceptions: severe financial hardship, terminal illness, permanent incapacity, or if you’re over 65. Some people use the First Home Super Saver Scheme to withdraw voluntary contributions for a home deposit, but that’s not the same as early access. Don’t rely on this as an emergency fund.

How do I know if I’m in the right super fund?

Look at three things: fees, performance, and insurance. Compare your fund’s annual fees to the industry average (around 1.2%). Then check its 5-year return against other funds on SuperRatings.com. Finally, review your life and disability insurance. Many default funds offer poor coverage at high cost. You can often get better insurance outside super.

Do I need to contribute extra if my employer already pays 12%?

Yes, unless you want a modest retirement. The 12% is designed to replace about 50% of your pre-retirement income. Most experts say you need 70-80% to live comfortably. That means you need to add your own money. Even $50 a week doubles your chances of retiring on your terms.

What happens to my super if I die before retirement?

Your super balance goes to your nominated beneficiary-usually a spouse, child, or dependent. If you haven’t nominated anyone, the trustee decides based on your family situation. It’s not part of your will unless you’ve made a binding nomination. Make sure you’ve updated your beneficiary details. Many people forget this until it’s too late.

If you’re wondering whether pension plans are worth it, the answer isn’t theoretical. It’s in your bank statement, your payslip, and your future self. The system isn’t flawless-but for the vast majority of Australians, it’s the single most powerful tool they have to build financial security. Start now. Don’t wait. Your future self will thank you.