Student Loan Credit Impact Calculator

How Your Student Loans Affect Your Credit Score

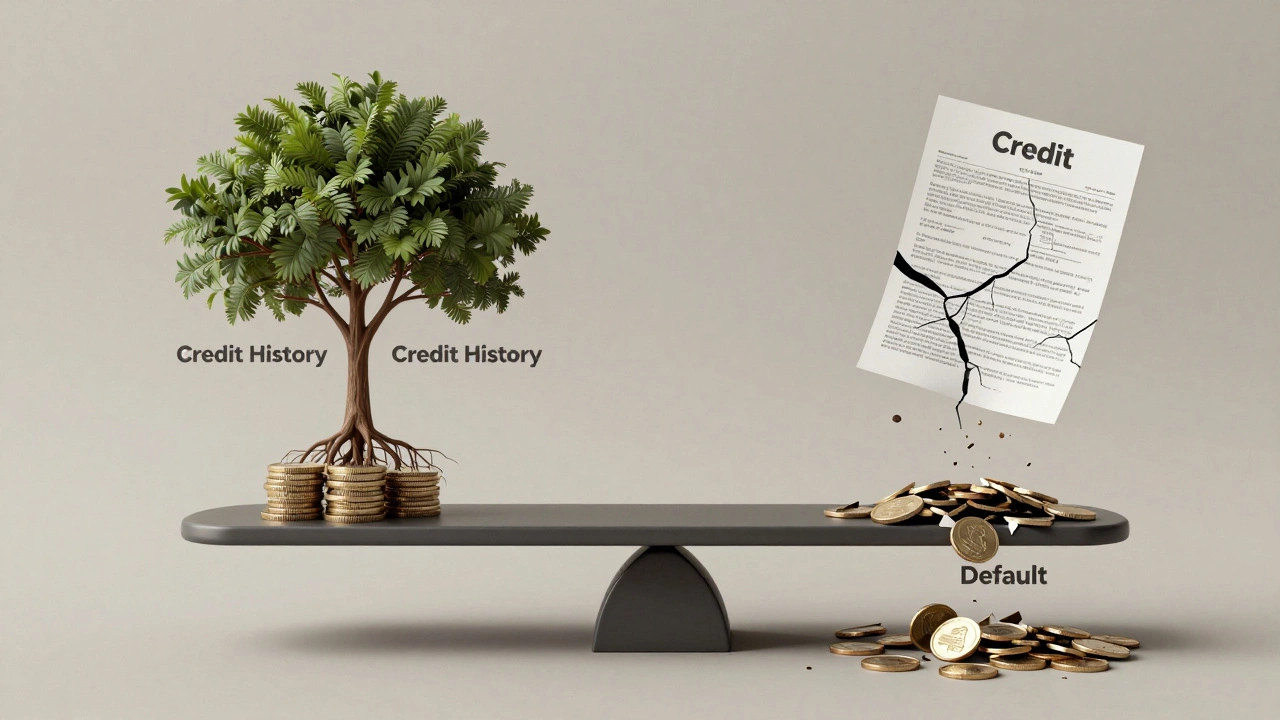

This calculator shows how your payment history impacts your credit score. Based on data from the Federal Reserve Bank of New York (2023), consistent payments can increase your score by 40 points within 2 years after graduation.

Your Credit Score Impact

Consistent on-time payments help build credit history and improve your score. Credit scoring models reward responsible payment behavior.

Key Insight

Missing just 3 payments can lower your score by 100 points or more. On-time payments show lenders you're reliable, which is crucial when applying for mortgages or car loans later.

Many students hear stories about student loans ruining credit scores, and it’s easy to believe they’re a financial trap. But the truth is more complicated. Student loans aren’t inherently bad for your credit-in fact, they can help build it. The real issue isn’t the loan itself, but how you manage it. If you make payments on time and keep your balance under control, student loans can be one of the best ways to start building credit. If you miss payments or default, then yes, they’ll hurt you. Let’s cut through the noise and look at what actually happens when you take out student loans.

Student loans help you build credit history

When you take out a student loan, that loan gets reported to credit bureaus. That means every on-time payment starts building your credit history. For someone with no credit, this is huge. Most young people start with zero credit history. Without a loan, credit card, or other account, lenders have no way to know if you’ll pay back money. A student loan changes that. It gives you a track record. In the U.S., about 70% of borrowers under 25 report that their student loan was their first line of credit. In Australia, where student debt is handled through the HECS-HELP system, repayments are tracked by the ATO and reported to credit agencies as part of your financial history.

Think of it like this: paying your student loan on time is like doing push-ups for your credit score. It doesn’t give you instant results, but over time, it makes you stronger. A 2023 study by the Federal Reserve Bank of New York found that borrowers who made consistent payments on their student loans saw their credit scores rise by an average of 40 points within the first two years after graduation. That’s enough to move you from ‘thin file’ to ‘prime borrower’ status.

Missed payments hurt-fast

But here’s the flip side. If you miss payments, the damage happens quickly. Late payments show up on your credit report after 30 days. After 90 days, the loan goes into delinquency. After 270 days of non-payment (in the U.S.), the loan defaults. Defaulting on a student loan is one of the worst things you can do to your credit. It stays on your report for seven years. Even if you later pay it off, the default mark doesn’t disappear.

In Australia, HECS-HELP debts don’t default in the same way. Repayments are automatically deducted from your income once you earn above the threshold (currently $51,550 for 2025-26). But if you’re working overseas and not reporting income, or if you’re on a payment plan and fall behind, your debt can still be flagged. Credit reporting agencies like Equifax and Experian may note your repayment behavior, especially if you’re using private lenders or international student loans.

High balances don’t hurt like credit cards do

One myth is that carrying a large student loan balance is bad for your credit. That’s not true-at least not the same way a maxed-out credit card is. Credit scoring models treat installment loans (like student loans) differently than revolving credit (like credit cards). Your credit utilization ratio, which is the percentage of your credit limit you’re using, doesn’t apply to student loans. So even if you owe $50,000, it won’t drag your score down just because the balance is high.

What matters more is your payment history and the length of your credit history. A $50,000 student loan with 10 years of on-time payments looks far better to lenders than a $5,000 credit card with three late payments. In fact, having a mix of credit types-including student loans-can improve your score. Credit scoring models reward people who handle different kinds of debt responsibly.

Forbearance and deferment aren’t automatic fixes

If you’re struggling to pay, you might think putting your loan on pause (forbearance or deferment) will protect your credit. It doesn’t. While these options stop your payments, they don’t stop the loan from being reported. If you’re in forbearance and your loan was already delinquent before you paused it, that delinquency stays on your report. Worse, some private lenders report forbearance as a sign of financial distress, which can lower your score.

In Australia, HECS-HELP doesn’t offer forbearance. If your income drops below the threshold, repayments stop automatically. That’s actually better for your credit because there’s no risk of missed payments. But if you’re using a private student loan from a bank or lender, check the terms. Some private lenders report paused payments as delinquent if you don’t formally apply for a hardship plan.

Defaulting has long-term consequences

Defaulting on a student loan is worse than defaulting on a car loan or credit card. The government can garnish your wages, seize tax refunds, and even withhold Social Security benefits (in the U.S.). In Australia, the ATO can deduct from future income, and your debt never goes away-even if you file for bankruptcy. And because student loans are reported to credit bureaus, defaulting tanks your credit score. You might not be able to rent an apartment, get a phone contract, or even qualify for a job that requires a credit check.

One real example: a 28-year-old in Melbourne defaulted on a private student loan in 2022. She couldn’t get a car loan two years later because her credit report showed a defaulted loan. Even though she paid it off in full in 2024, the default stayed on her report until 2029. That’s five years of being treated like a high-risk borrower.

How to use student loans to build credit

- Make every payment on time-set up autopay if you can.

- Don’t skip payments just because you’re in school. Even small payments help.

- Keep track of your loan servicer and repayment terms. Know when grace periods end.

- If you’re in Australia, make sure your income is reported to the ATO. That ensures your HECS-HELP repayments are accurate and recorded.

- Check your credit report once a year. In Australia, you can get free reports from Equifax and Illion.

Using student loans wisely means treating them like a tool, not a burden. They’re not a shortcut to wealth, but they can be a solid foundation for your financial future-if you handle them right.

What if you can’t afford your payments?

Don’t panic. Ignoring the problem makes it worse. In the U.S., income-driven repayment plans cap your monthly payment at a percentage of your income. In Australia, HECS-HELP already does this-you only pay when you earn above $51,550. If your income drops, your payment drops to zero. No penalty. No credit hit.

For private loans, contact your lender as soon as you think you’ll miss a payment. Many offer hardship programs, temporary reductions, or extended terms. Ask for a repayment plan. Don’t wait until you’re 60 days late. The sooner you act, the less damage you’ll do to your credit.

Do student loans hurt your credit score if you pay them on time?

No, student loans don’t hurt your credit score if you pay them on time. In fact, they help. On-time payments build a positive payment history, which is the biggest factor in your credit score. Many people with no prior credit history use student loans to start building credit.

Can student loans improve your credit mix?

Yes. Credit scoring models reward people who manage different types of debt. Student loans are installment loans, while credit cards are revolving debt. Having both shows lenders you can handle different financial responsibilities. A good credit mix can add a few points to your score.

Does deferment or forbearance hurt your credit?

Not if it’s approved properly. If you’re granted deferment or forbearance and you’re current on your payments before pausing, it won’t hurt your credit. But if you were already late, those late marks stay. Some private lenders may report forbearance as a negative, so always confirm how your lender reports it.

Do student loans show up on credit reports?

Yes. Both federal and private student loans are reported to credit bureaus. In Australia, HECS-HELP repayments are tracked by the ATO and can appear on your credit file, especially if you’re using private lenders or have missed repayments while overseas.

Can you remove student loans from your credit report?

Only if they’re reported in error. Once paid, the loan will still appear on your report for up to 10 years, but it will show as "paid" or "closed." A default stays for seven years. You can’t remove accurate, on-time payment history-it’s a positive record.

Is it better to pay off student loans early?

It depends. Paying early saves you interest, but it doesn’t necessarily boost your credit score. In fact, keeping the loan open and making consistent payments over time can help your score more than paying it off quickly. If you’re aiming to build credit, keeping the loan active and paid on time for the full term is often better than rushing to pay it off.

Final thought: It’s about control, not avoidance

Student loans aren’t good or bad. They’re neutral. They become harmful only when you lose control. If you understand your repayment terms, make payments on time, and communicate with your lender when things get tough, they can be one of your best financial tools. The goal isn’t to avoid debt-it’s to manage it well. That’s how you build real credit.