Student Loan Forgiveness & Tax Estimator

Your Projection

-- Payments Required

Estimated Tax Bill at Forgiveness

Based on a --% federal tax rate applied to the full balance.

Enter your details to see when your loans might be forgiven and what the tax impact could be.

It is a common myth that every student loan disappears into thin air after two decades. If you are holding onto this belief, you might be walking into a financial trap. The short answer is no. Not all student loans get forgiven after 20 years. In fact, for most borrowers, the clock only starts ticking if you meet very specific criteria involving how you pay your bills.

The confusion stems from the existence of Income-Driven Repayment (IDR) plans. These federal programs do offer forgiveness, but they come with strict rules, tax implications, and eligibility requirements that many people overlook. Meanwhile, private lenders operate under completely different laws where "forgiveness" is rarely part of the contract unless you die or become permanently disabled.

Key Takeaways

- Federal loans only: Private student loans generally do not have any forgiveness program after 20 years.

- Plan matters: You must be enrolled in an Income-Driven Repayment (IDR) plan to qualify for forgiveness.

- Timeline varies: Most borrowers get forgiveness after 20 years (240 payments), but those with only undergraduate loans may qualify after 10 years.

- Tax consequences: Forgiven amounts are typically considered taxable income by the IRS, creating a large bill at the end.

- Credit impact: Carrying these loans for decades can hurt your credit score due to high utilization and long-term debt history.

How Federal Loan Forgiveness Actually Works

To understand why your loan might not vanish, we need to look at the mechanism behind it. The United States Department of Education offers several Income-Driven Repayment (IDR) plans. These plans cap your monthly payment at a percentage of your discretionary income-usually between 5% and 10%. Because the payments are often lower than what accrues in interest, the balance grows slowly or stays flat. To compensate for this, the government forgives the remaining balance after a set period.

However, this safety net is exclusive to Federal Direct Loans. If you borrowed money through a bank, credit union, or online lender, you are out of luck. Private lenders are businesses. They lend money to make a profit. They do not have a legal obligation to wipe your slate clean after 20 years. If you stop paying a private loan, they will sue you, garnish your wages, and damage your credit for life. There is no automatic expiration date on private debt.

Even within the federal system, not all loans qualify. Older FFEL Program loans or Perkins Loans must usually be consolidated into a Direct Consolidation Loan before they count toward IDR forgiveness. If you haven't taken this administrative step, your payments might not even be counting toward the 240-payment goal.

The 20-Year vs. 25-Year Rule

You heard "20 years," but did you know it could be 25? The timeline depends entirely on the type of degree you pursued. This distinction is crucial for planning your exit strategy.

| Loan Composition | Forgiveness Timeline | Total Payments Required |

|---|---|---|

| Undergraduate Loans Only | 10 Years | 120 Payments |

| Graduate or Professional Loans | 25 Years | 300 Payments |

| Mixed Undergraduate & Graduate | 20 Years | 240 Payments |

If you only took out loans for your bachelor's degree, you are looking at a 10-year horizon. But if you went to law school, medical school, or got an MBA, the clock stretches to 25 years. Most students fall into the mixed category, hence the popular "20-year" rumor. It is vital to check your loan servicer's portal to see exactly which bucket you fall into. Guessing can cost you thousands in unnecessary interest payments.

The Hidden Cost: Taxes on Forgiven Debt

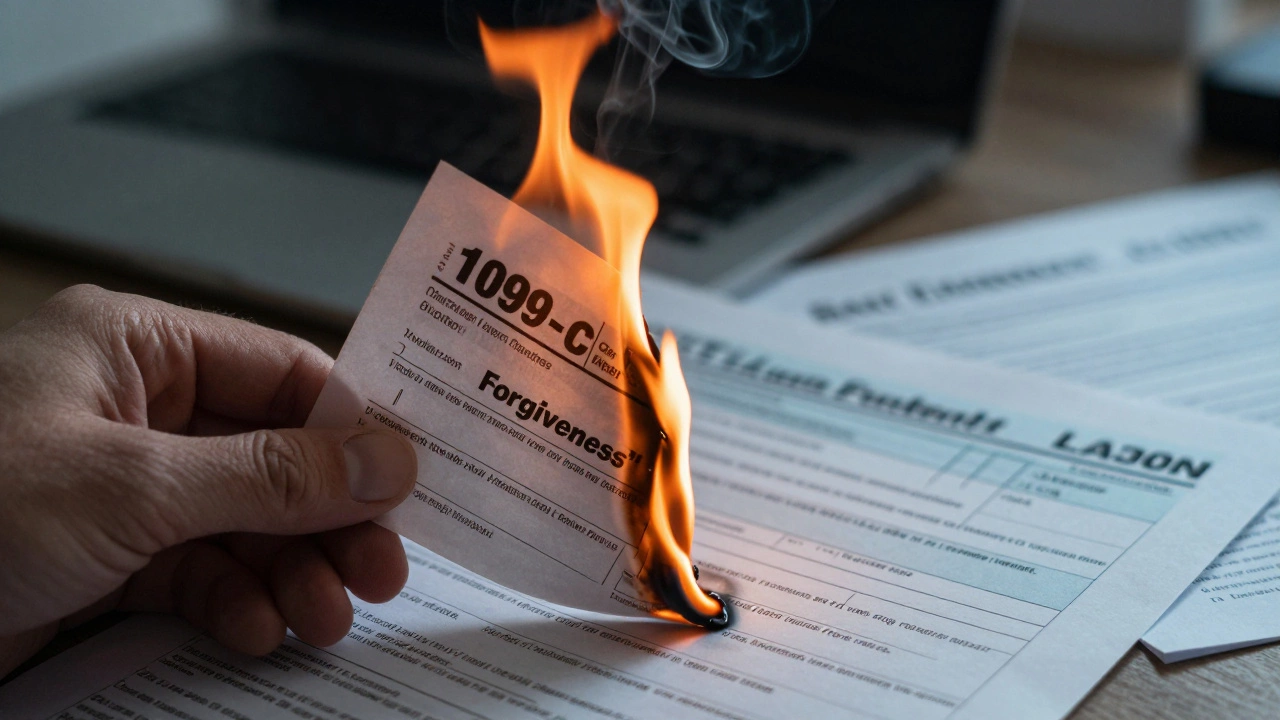

Here is the part that catches almost everyone off guard. When the government forgives your loan, they consider that forgiven amount as Taxable Income. Why? Because the IRS views debt cancellation as a form of earnings. If you owed $80,000 and it gets wiped out, the IRS thinks you just made $80,000.

This means you will receive a 1099-C form in the mail, and you must report that income on your tax return. Depending on your tax bracket, you could face a massive tax bill in the year your loan is forgiven. Many borrowers find themselves in a worse financial position right when their debt disappears because they cannot afford the lump-sum tax payment.

There was a temporary waiver for tax-free forgiveness during the pandemic era (up to December 2025), but as of 2026, standard tax rules apply again. Unless new legislation passes to permanently exempt student loan forgiveness from taxes, you must budget for this eventuality. Some financial advisors recommend setting aside a small portion of each month’s savings specifically for this future tax liability.

Why Private Loans Are Different

Let’s talk about Private Student Loans. These loans are governed by state contract law, not federal statute. When you sign up for a private loan, you agree to a fixed or variable interest rate and a repayment term, typically 5 to 20 years. Unlike federal loans, there is no "pay what you can" option based on your salary.

If you lose your job or your income drops, a private lender does not care. Your payment remains the same. If you default, the consequences are severe. Private lenders can pursue legal judgment against you. They can seize assets if your state allows it. They can garnish your wages without the due process protections afforded to federal borrowers.

Is there any way to get private loans forgiven? Generally, no. The only exceptions are death and total and permanent disability (TPD). Some private lenders have TPD discharge programs, but they require extensive medical documentation and are not automatic. Bankruptcy is another avenue, but discharging student loans in bankruptcy is notoriously difficult. You must prove "undue hardship," a high legal bar that few courts are willing to clear. So, if you have private loans, the 20-year rule does not save you. You owe that money until it is paid off or you die.

The Credit Score Impact of Long-Term Debt

Staying in an IDR plan for 20 or 25 years isn't just a cash-flow issue; it affects your credit health. Credit scoring models like FICO look at your debt-to-income ratio and the age of your accounts. A large student loan balance that never decreases can signal risk to other lenders.

When you apply for a mortgage or a car loan, the bank looks at your monthly obligations. Even if your IDR payment is low, the sheer size of the remaining balance can worry underwriters. More importantly, carrying debt for two decades keeps your average age of credit history complex. While a long history is good, a history of persistent, unpaid principal is not ideal. Once the loan is forgiven and closed, your credit score might actually dip temporarily because you lost a long-standing account. However, the removal of the monthly payment obligation usually helps your overall financial flexibility more than it hurts your score.

Alternatives to Waiting 20 Years

If the idea of waiting two decades makes you anxious, you are not stuck. There are ways to accelerate payoff or eliminate debt faster.

- Public Service Loan Forgiveness (PSLF): If you work for a government agency or a non-profit organization, you can qualify for forgiveness after just 10 years (120 payments). This applies to both undergraduate and graduate loans. You must be on an IDR plan and working full-time for a qualifying employer.

- Refinancing: If you have a stable, high income, refinancing your federal loans into a private loan with a lower interest rate can save thousands. However, this is a one-way street. You lose access to IDR and forgiveness forever. Only do this if you are confident you can pay off the loan before the 20-year mark.

- Bonus Payments: Any extra money-tax refunds, work bonuses, holiday gifts-can go toward the principal. Since IDR payments are often low, throwing extra cash at the loan reduces the balance that would otherwise be forgiven (and taxed).

Common Mistakes Borrowers Make

Many people fail to get their loans forgiven not because they aren't eligible, but because of administrative errors. Here are the pitfalls to avoid:

- Missing a Payment: You need 120 or 240 *qualifying* payments. If you miss a month, you don't just lose that month; you might have to restart the count depending on the plan and servicer policies. Always pay on time.

- Switching Servicers Without Confirmation: The Department of Education changes loan servicers frequently. When you switch, verify that your previous payments were counted. Disputes over missing credits are common and can delay forgiveness by years.

- Ignoring Annual Recertification: IDR plans require you to update your income and family size every year. If you skip this, you might be placed on a higher payment plan or lose your IDR status entirely, resetting your progress.

- Mixing Up Plans: Making payments on a Standard Repayment Plan does not count toward IDR forgiveness. You must be actively enrolled in an IDR plan like SAVE, PAYE, IBR, or ICR.

What Should You Do Right Now?

First, log into your federal loan servicer’s website. Check which repayment plan you are currently on. If it says "Standard" or "Extended," you are not on track for forgiveness. Switch to an IDR plan immediately. Every month counts.

Second, separate your federal and private loans mentally. Create a spreadsheet. For federal loans, calculate your projected forgiveness date. For private loans, create a aggressive payoff plan. Do not assume private loans will disappear.

Third, consult a tax professional. Ask them about strategies to mitigate the tax hit when forgiveness occurs. Can you adjust your withholding? Can you invest the difference between your low IDR payment and your actual ability to pay in a tax-advantaged account?

Finally, stay informed. Student loan policy is volatile. Laws change. As of 2026, the SAVE plan is the most popular IDR option, offering $0 payments for some borrowers and capping interest capitalization. Keep an eye on news from the Department of Education. Policies that exist today might be modified tomorrow.

Does the 20-year forgiveness rule apply to private student loans?

No. Private student loans are contracts with banks or lenders and do not have any federal forgiveness programs. You are responsible for repaying the full amount plus interest until the loan is paid off, discharged due to death/disability, or potentially through bankruptcy (which is very difficult).

Is forgiven student loan debt really taxable?

Yes, as of 2026, debt forgiven through Income-Driven Repayment plans is considered taxable income by the IRS. You will receive a 1099-C form and must pay income tax on the forgiven amount in the year it is discharged. This can result in a significant tax bill.

How many payments do I need for forgiveness if I have graduate loans?

If you have any graduate or professional loans, you typically need to make 300 qualifying monthly payments, which equals 25 years. If you have only undergraduate loans, you need 120 payments (10 years). Mixed loans usually require 240 payments (20 years).

Can I refinance my federal loans to pay them off faster?

Yes, you can refinance federal loans with a private lender. This often lowers your interest rate and monthly payment. However, once you refinance, you lose all federal benefits, including access to Income-Driven Repayment and forgiveness. This is irreversible.

What happens if I miss a payment on an IDR plan?

Missing a payment can disrupt your progress toward forgiveness. Depending on the specific plan and servicer, you may need to bring the account current before your next payment counts. Consistent, on-time payments are critical to staying on track for the 120, 240, or 300-payment requirement.