Pension Death Benefit Tax Calculator

Enter Details

Estimated Outcome

It is a question nobody wants to ask while they are healthy and working. But when you pass away, your pension doesn't just vanish into thin air. For many families, it represents a significant financial legacy. However, how that money gets to them depends entirely on the type of pension you hold, whether you had already started taking money out, and who you named as your beneficiaries.

If you get these details wrong, your loved ones could face a hefty tax bill or worse, nothing at all. The rules for pension payouts after death are strict, but they also offer one of the few opportunities in the UK to leave a substantial sum to your family free from Inheritance Tax (IHT). Let's break down exactly what happens to your savings when you die, so you can protect your family's future.

The Critical Factor: Did You Start Drawing Income?

The single biggest factor determining what happens to your pension is your age and status at the time of death. Specifically, were you under or over 75, and had you already started accessing your funds? This distinction creates two very different outcomes for your beneficiaries.

If you die before turning 75, your pension pot is generally passed on free of income tax. Your beneficiaries can take the lump sum or draw an income without paying any additional tax on those withdrawals. This makes pre-75 death benefits one of the most tax-efficient ways to leave money to your children or spouse.

If you die after turning 75, the situation changes slightly. Your beneficiaries can still inherit the pension, but they will need to pay income tax on any withdrawals they make. The tax is charged at their marginal rate-so if they are a basic rate taxpayer, they pay 20%; if they are a higher rate taxpayer, they pay 40%. Crucially, this money does not go through your estate, meaning it is usually exempt from Inheritance Tax.

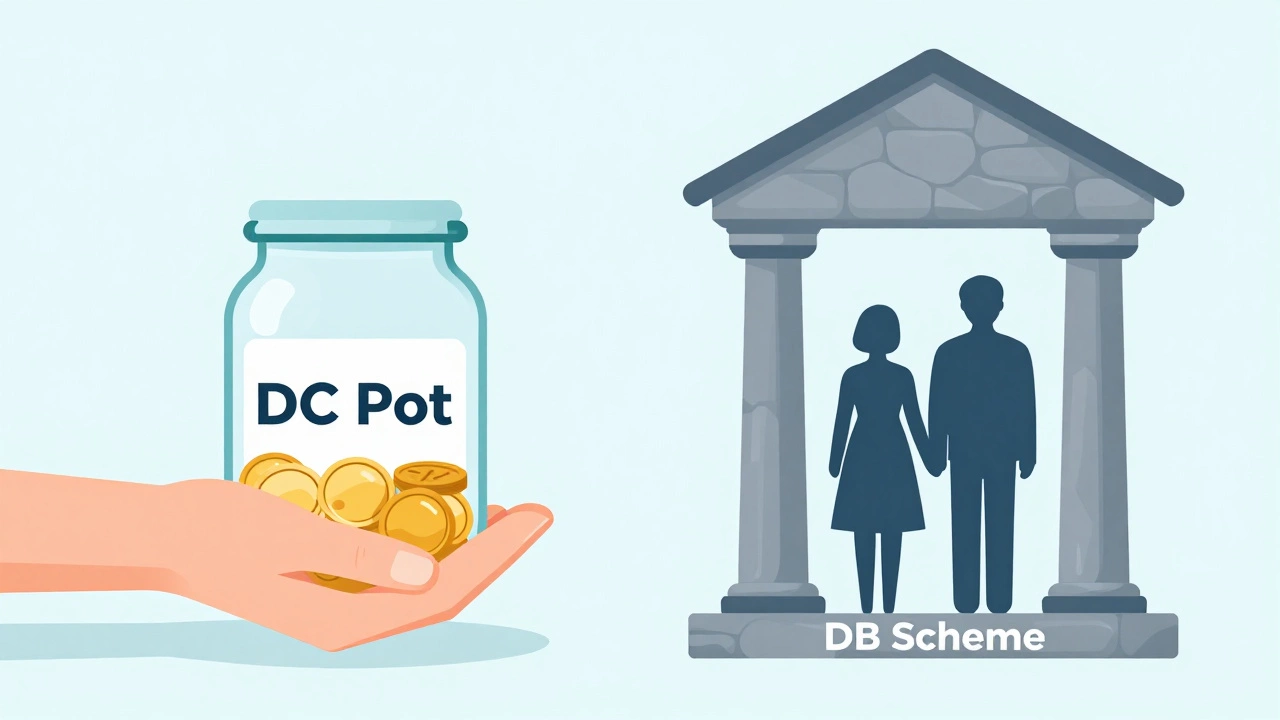

Defined Contribution vs. Defined Benefit Pensions

Not all pensions work the same way. Most people today have a defined contribution (DC) pension, such as a workplace auto-enrolment scheme or a private SIPP. These are pots of money that grow based on investment performance. When you die, the remaining balance is paid out to your nominated beneficiaries.

However, older generations often hold defined benefit (DB) pensions, typically final salary schemes from local government or large corporations. These work differently because they promise a specific income for life rather than holding a cash pot. If you die before retiring with a DB scheme, the provider usually pays a lump-sum death benefit, often calculated as three times your final salary. If you die while already receiving the pension, the scheme may continue paying a reduced amount to your spouse or civil partner, known as a survivor’s pension.

| Feature | Defined Contribution (DC) | Defined Benefit (DB) |

|---|---|---|

| What is inherited? | Remaining cash pot value | Lump sum or survivor's income |

| Tax if under 75 | Tax-free | Usually tax-free |

| Tax if over 75 | Beneficiary pays income tax | Beneficiary pays income tax |

| Inheritance Tax (IHT) | Exempt (if nominated correctly) | Exempt (usually) |

| Control | You nominate beneficiaries | Trustee discretion applies |

The Power of the Expression of Wish Form

Here is where many people make a costly mistake. They assume their pension will automatically go to their spouse or children because it is written in their will. It won’t. Pensions are not part of your estate. Instead, they are governed by a separate document called an "Expression of Wish" or "Nomination of Beneficiaries" form.

This form tells the pension provider who you would like to receive your money. While providers are not legally bound to follow this wish-they technically decide based on who has a financial dependency on you-they almost always do if the form is up to date. If you don’t fill this out, the provider has to guess, which can lead to delays, arguments among family members, or the money going to someone you didn’t intend.

You should review this form every time your circumstances change. Got married? Divorced? Had a child? Moved in with a partner? Update the form immediately. An old form naming an ex-spouse could cause significant legal headaches and heartbreak for your current family.

What Happens If You Die Before Retirement Age?

Dying young is tragic, but financially, it offers the best outcome for your heirs regarding pensions. If you die before reaching your normal minimum retirement age (currently 55, rising to 57 in April 2028), your entire pension pot is usually paid out tax-free to your beneficiaries.

Your beneficiaries have several options here. They can:

- Take the whole amount as a lump sum.

- Transfer the money into their own name as an inherited pension, allowing it to grow tax-free until they reach retirement age themselves.

- Set up a joint life annuity that starts paying out now.

Transferring the pot into their own name is often the smartest move. It allows the investments to continue growing without immediate tax pressure, effectively giving your children or spouse a head start on their own retirement savings.

Paying Off Debts With Your Pension Pot

A common misconception is that your pension can be used to pay off your debts after you die. Generally, it cannot. Because the pension is not part of your estate, creditors cannot claim against it to settle unpaid bills, mortgages, or loans.

However, there is a nuance. If you had already started drawing an income from your pension (like a drawdown plan) and left some money in the account, that remaining balance might be considered part of your estate if no beneficiaries were nominated. In that specific case, it could be used to pay debts. But for the vast majority of people with untouched DC pots, the money goes straight to the beneficiaries, bypassing your creditors entirely.

Survivor’s Benefits and Annuities

If you converted your pension pot into an annuity-a guaranteed income for life-the rules depend on the type of annuity you bought. Many people buy a "single life" annuity, which stops paying the moment they die. In this case, there is nothing left for beneficiaries unless they purchased optional guarantees.

To protect your family, you can add riders to your annuity contract. For example, a "guaranteed period" ensures payments continue for five or ten years even if you die early. A "joint life" annuity continues paying your spouse for the rest of their life, though the monthly amount is usually lower to account for the longer payout period. Always check your annuity contract to see what protections are in place.

Common Pitfalls to Avoid

Planning for pension death benefits seems straightforward, but small errors can have big consequences. Here are the most common mistakes:

- Failing to update nominations: As mentioned, an outdated form is the number one cause of disputes. Review it annually.

- Ignoring State Pension: The UK State Pension does not pass to beneficiaries. However, your spouse may be able to inherit up to 50% of your accrued State Pension credit if you died before claiming it, provided you met certain National Insurance conditions.

- Mixing up estates: Remember, your pension is likely separate from your house and savings. Don’t assume your executor handles everything.

- Not considering tax implications for high earners: If your beneficiary is a higher-rate taxpayer, inheriting a large pension pot after you turn 75 could push them into a higher tax bracket when they withdraw the funds.

Next Steps for Protecting Your Family

Don’t wait until it’s too late. Take these steps today to ensure your pension serves your family’s needs:

- Locate your policies: Find all your pension statements, including old workplace schemes you may have forgotten about.

- Contact the providers: Call each provider and ask for an updated Expression of Wish form. Fill it out accurately.

- Review your annuity options: If you are close to retirement, consider whether a joint-life annuity or a drawdown plan with clear beneficiary instructions is better for your spouse.

- Talk to your beneficiaries: Make sure your family knows where the documents are and who to contact. Silence can lead to missed deadlines and lost benefits.

Your pension is more than just retirement income; it’s a potential lifeline for those you leave behind. By understanding how payouts work and taking simple administrative steps, you can ensure that your hard-earned savings provide security rather than stress.

Does my pension go to my next of kin automatically?

Not necessarily. While providers often default to next of kin if no instructions are given, they have discretion. Without a valid Expression of Wish form, the process can be slow and uncertain. It is crucial to nominate beneficiaries explicitly to avoid delays or unintended recipients.

Is pension money subject to Inheritance Tax?

Generally, no. Money held in a pension fund is outside of your estate for Inheritance Tax purposes, provided it is paid directly to beneficiaries via a trust arrangement. This makes pensions one of the most tax-efficient assets to leave behind, especially compared to cash savings or property.

Can my children inherit my pension if I am over 75?

Yes. Your children can inherit your pension pot regardless of your age. However, if you die after turning 75, they will need to pay income tax on any withdrawals they make from the inherited pot. The tax rate depends on their personal income level.

What happens to my pension if I die in debt?

Your pension pot is typically protected from creditors. Since it is not part of your estate, lenders cannot seize it to repay outstanding debts. The money goes directly to your nominated beneficiaries, shielding it from your financial liabilities.

Do I need a solicitor to handle pension death claims?

Usually, no. Most pension providers have straightforward processes for claiming death benefits. Executors or beneficiaries simply need to submit proof of death and the completed claim forms. Legal help is only needed if there is a dispute among beneficiaries or complex trust issues.