$36,000 Loan Cost Calculator

Adjust Loan Parameters

Estimated Repayment

Monthly Payment

Total Principal

Total Interest

Total Amount Repaid

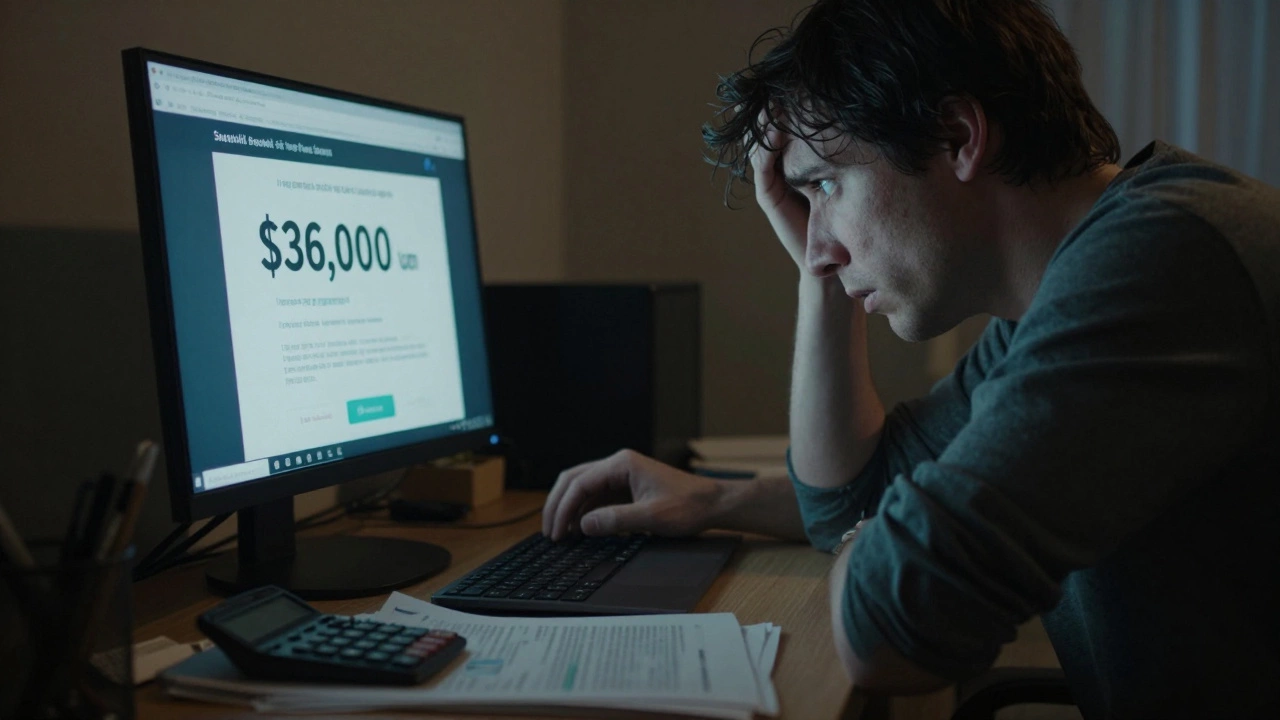

Imagine this: you’re staring at a stack of unpaid bills, your car needs repairs, and then an email pops up. It promises a financial hardship loan for exactly $36,000. The terms look too good to be true-low interest, instant approval, no credit check required. Your heart races. Is this finally the lifeline you’ve been waiting for? Or is it a trap designed to drain what little savings you have left?

The short answer is: if it sounds perfect, it’s almost certainly a scam. In the world of lending, especially when dealing with large sums like $36,000, there are very few "easy" buttons. Most legitimate lenders require rigorous checks, collateral, or a strong credit history. When you see offers that bypass these standard safeguards, you need to pause and investigate before you click "apply."

While we focus on protecting your finances here in Sydney and beyond, it’s worth noting that financial stress can manifest differently depending on where you are. For instance, someone dealing with international business travel might encounter different types of high-pressure sales tactics or even unrelated directories while searching for solutions online; checking resources like this directory is completely unrelated to finance but shows how easily one can stumble upon irrelevant or suspicious links during desperate internet searches. Always stay focused on verified financial institutions.

Red Flags That Signal a Fake Lender

Scammers are getting smarter, but they still rely on urgency and secrecy. Here are the biggest warning signs that a $36,000 hardship loan offer is fraudulent:

- Upfront Fees: This is the number one rule of lending. No legitimate lender will ask you to pay money before you receive the loan. If they ask for an "insurance fee," "processing fee," or "tax payment" via gift cards, wire transfer, or cryptocurrency, run away. Real lenders deduct fees from the loan amount or add them to the repayment schedule.

- Guaranteed Approval: If a company claims they approve everyone regardless of credit score, income, or employment status, they are lying. Every legitimate lender assesses risk. A $36,000 loan is significant capital; banks and credit unions will always verify your ability to repay.

- Poor Communication: Check the website’s contact information. Does it have a physical address? A working phone number? Or just a generic contact form and a Gmail/Yahoo email address? Legitimate companies have professional customer service channels.

- Pressure Tactics: Scammers create artificial deadlines. "Apply within 24 hours or lose this rate!" Real lenders understand that taking out a large loan is a serious decision and give you time to review the contract.

How Legitimate Hardship Loans Actually Work

So, if the easy offers are scams, how do people actually get help during financial crises? There are legitimate paths, but they require patience and honesty.

Bank Overdraft Protection is a safety net linked to your savings account or credit line that prevents bounced checks. Many people forget they already have this option. Before applying for new debt, call your current bank. They may offer a temporary increase in your overdraft limit or a small personal loan at a lower rate than external lenders because they know your history.

Credit Union Loans are member-owned financial cooperatives that often offer lower interest rates and more flexible terms than big banks. Credit unions are not-for-profit, which means their goal isn't to maximize profit from your interest payments. They are often more willing to work with members who are facing genuine hardships, such as job loss or medical emergencies. You’ll need to be a member (which usually costs a small annual fee), but the savings on a $36,000 loan can be thousands of dollars over the life of the loan.

Secured Personal Loans are loans backed by collateral like a car, home equity, or savings account. If you own assets, you can use them as security. Because the lender has something to seize if you default, they charge lower interest rates. However, this comes with risk: if you can’t repay, you lose the asset. Never put your primary residence at risk unless you are absolutely certain you can make the payments.

The Hidden Costs of "Easy" Money

Even if you find a lender that seems legitimate but offers unusually high-interest rates, you need to calculate the true cost. A $36,000 loan at 10% APR over five years looks manageable. But at 25% APR (common for subprime borrowers), the total interest paid could exceed $15,000. At 40% APR (typical for payday or title loans), you could end up paying double or triple the original amount.

Here’s a quick comparison table to show how interest rates impact your total repayment:

| Interest Rate (APR) | Monthly Payment | Total Interest Paid | Total Amount Repaid |

|---|---|---|---|

| 5% | $678 | $4,680 | $40,680 |

| 10% | $762 | $9,720 | $45,720 |

| 20% | $938 | $19,800 | $55,800 |

| 30% | $1,076 | $28,560 | $64,560 |

As you can see, jumping from a 10% to a 30% rate adds nearly $20,000 to your debt burden. That’s money you could have used for rent, groceries, or rebuilding your emergency fund. Always ask for the Annual Percentage Rate (APR), not just the monthly payment. The APR includes all fees and gives you the true cost of borrowing.

Alternatives to Taking Out a Large Loan

Before you sign anything, consider these alternatives that might solve your immediate problem without adding long-term debt:

- Negotiate with Creditors: Call your utility companies, landlords, and credit card issuers. Explain your situation. Many have hardship programs that allow you to defer payments, reduce interest temporarily, or set up a custom repayment plan. They would rather get paid slowly than not at all.

- Sell Unused Assets: Do you have electronics, furniture, or a second car? Selling items you don’t need can raise cash quickly without interest charges. Online marketplaces make this easier than ever.

- Government Assistance Programs: Depending on your location, there may be grants or low-interest loans available for specific hardships like medical bills, home repairs, or education. In Australia, organizations like Beyond Blue or local council services can provide guidance. In the US, look into state-specific emergency assistance funds.

- Non-Profit Credit Counseling: Agencies like the National Foundation for Credit Counseling (NFCC) in the US or similar bodies in other countries offer free or low-cost advice. They can help you create a budget, negotiate with creditors, and explore debt management plans.

What to Do If You’ve Already Been Scammed

If you’ve already sent money or shared personal information with a fake lender, act immediately:

- Contact Your Bank: If you wired money or used a debit card, call your bank right away. While it’s often difficult to reverse wire transfers, they may be able to flag the transaction or freeze your account to prevent further losses.

- Change Your Passwords: If you shared your Social Security number, date of birth, or banking login details, change those passwords immediately. Enable two-factor authentication on all your accounts.

- Place a Fraud Alert: Contact one of the major credit bureaus (Equifax, Experian, TransUnion) to place a fraud alert on your credit report. This makes it harder for scammers to open new accounts in your name.

- Report the Crime: File a report with your local police department and relevant consumer protection agencies. In the US, report to the Federal Trade Commission (FTC). In Australia, report to the Australian Competition and Consumer Commission (ACCC) or Scamwatch.

Frequently Asked Questions

Can I get a $36,000 loan with bad credit?

It is possible, but you will face higher interest rates and stricter requirements. Look for secured loans (backed by collateral) or co-signers with good credit. Avoid unsecured personal loans from predatory lenders, as the costs can be unsustainable.

Are financial hardship loans tax-deductible?

Generally, no. Personal loan interest is not tax-deductible unless the loan is used for specific purposes like buying a rental property or starting a business. Consult a tax professional for advice tailored to your situation.

How long does it take to get approved for a hardship loan?

Legitimate lenders typically take 1-3 business days to process applications, including credit checks and document verification. If a lender promises same-day or instant approval without any documentation, it is likely a scam.

What documents do I need to apply for a large personal loan?

Expect to provide proof of identity (driver’s license/passport), proof of income (pay stubs/tax returns), proof of employment, and bank statements. Lenders need to verify your ability to repay the loan.

Is it safe to apply for multiple loans at once?

Applying to multiple lenders within a short period (usually 14-45 days) results in only one hard inquiry on your credit report, so it won’t significantly hurt your score. However, ensure you compare offers carefully and avoid submitting incomplete applications that trigger unnecessary inquiries.