Defined Benefit Pension Overview

When working with Defined Benefit, a pension plan that promises a set monthly income in retirement, calculated from final salary and years of service. Also known as DB pension, it relies on employer funding and actuarial assumptions to guarantee payments. In the broader Pension system, defined benefit schemes sit alongside defined contribution plans and state benefits, offering the security of a predictable cash flow after you stop working. This predictability creates a direct semantic link: defined benefit encompasses a promised income, requires employer contributions, and influences how you shape your overall retirement strategy.

Key Factors that Shape a Defined Benefit Plan

Understanding a defined benefit scheme means looking at Retirement Planning the process of estimating future income needs, managing assets, and aligning them with expected pension benefits. A solid retirement plan will factor in the guaranteed income from a DB pension, then layer additional savings, debt‑reduction tactics, and potential equity release moves. Employer‑Sponsored Pension any retirement plan offered by a company, including defined benefit and defined contribution options adds another layer: the quality of the employer’s funding status directly affects the security of your future cash flow. When you combine this with Cash Flow Management the practice of tracking income and expenses to ensure you can meet short‑term needs while preserving long‑term goals, you get a clear picture of how much of your budget can be devoted to mortgage payments, debt consolidation, or building an emergency fund. These entities interrelate: effective cash flow management supports retirement planning, which in turn determines whether you can comfortably rely on a defined benefit payout without needing risky equity‑release loans or high‑interest credit cards.

Putting all these pieces together gives you a practical roadmap. If you have a defined benefit pension, you can often afford a larger mortgage or a shorter loan term because the guaranteed income reduces lender risk. Conversely, if the DB scheme is underfunded, you might want to prioritize debt‑consolidation loans, protect your credit score, or explore budgeting tricks like the 3 R’s (Reality, Reserve, Review) to build a safety net. The articles below dive into checking‑account balances, home‑equity loan pitfalls, debt‑consolidation options, and smart budgeting methods—all of which help you make the most of a defined benefit pension while keeping your overall financial picture healthy. Ready to see how these ideas play out in real‑world scenarios? Scroll down to explore the full collection of guides tailored for anyone with a DB pension or anyone looking to tighten their money game.

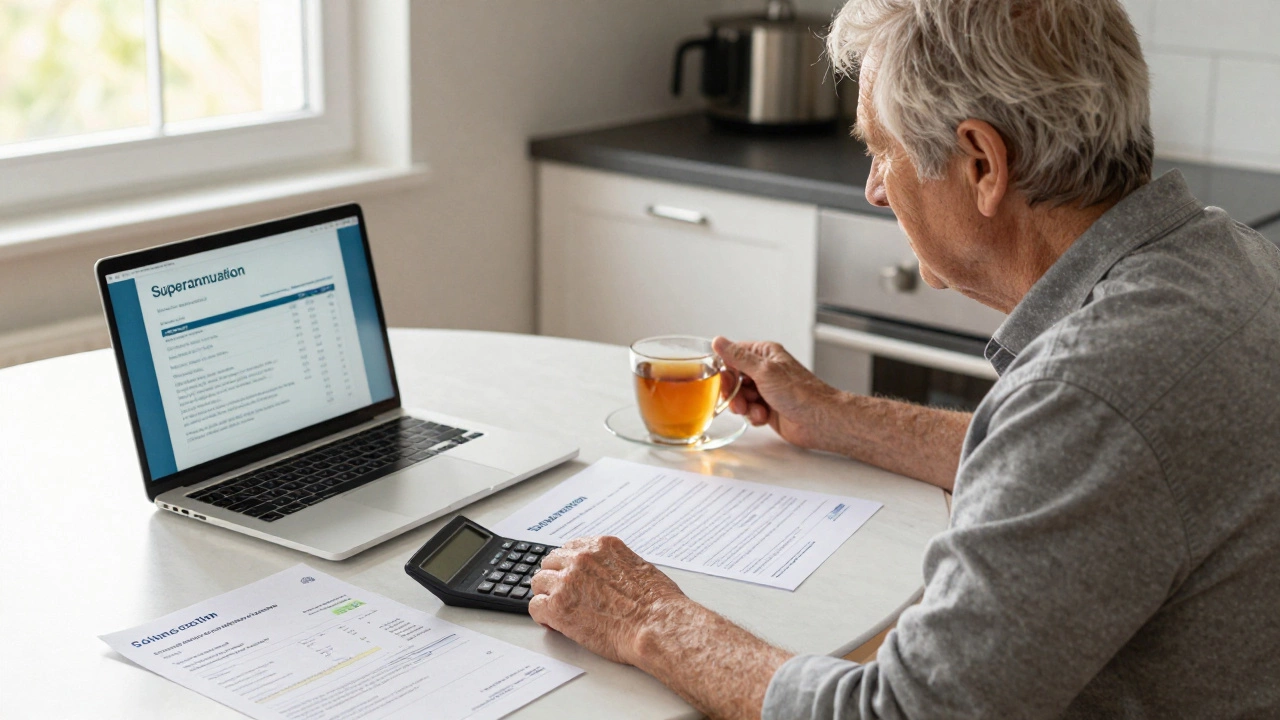

Are Pension Plans Obsolete in 2026?

Pension plans aren't obsolete-but they're not enough anymore. Superannuation is just the start. In 2026, you need multiple income streams to retire comfortably. Here's how to build one.

Read More >>Pension vs 401(k): Which Retirement Plan Wins?

Explore the core differences between pensions and 401(k) plans, covering guarantees, taxes, risk, and real‑world examples to help you pick the right retirement strategy.

Read More >>