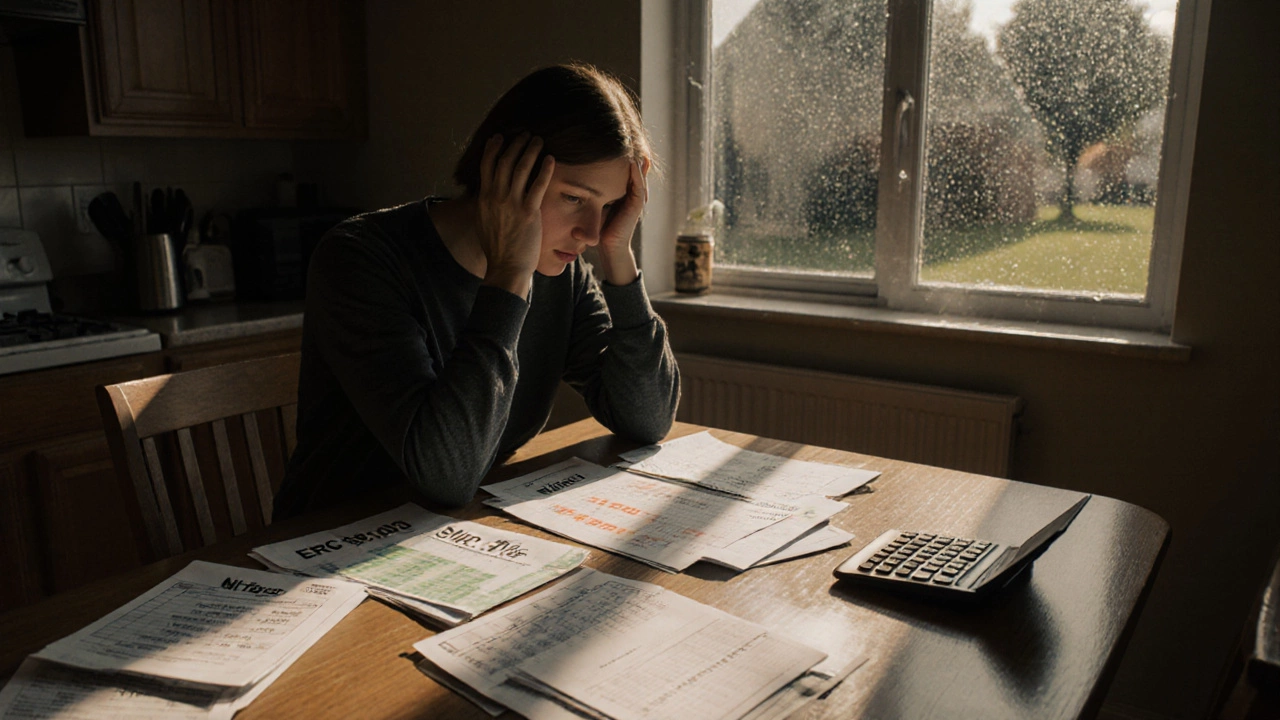

Home Loan Refinancing Dangers: What You Must Know Before You Switch

When you think about home loan refinancing, the process of replacing your current mortgage with a new one, often to get a lower rate or access cash. Also known as remortgaging, it sounds like a smart move—until you realize how many people end up worse off. It’s not magic. It’s a financial tool, and like any tool, it can cut both ways. Many think refinancing means instant savings, but the truth is, it often comes with hidden fees, longer terms, and traps that quietly eat away at your equity.

One of the biggest dangers is equity release, pulling cash out of your home’s value during refinancing. It feels like free money, but you’re not getting a gift—you’re borrowing against your future. Every pound you take out increases your total debt, and if property values drop, you could end up owing more than your home is worth. And if you’re tempted by a low introductory rate, remember: those rates don’t last. The mortgage switching, the act of changing lenders to get better terms. Also known as remortgaging, it often comes with arrangement fees, valuation costs, and legal charges that can add thousands to your bill. Some people refinance just to lower their monthly payment, but stretch their loan from 20 to 30 years. That means you pay more in interest over time—even if the monthly number looks better.

Then there’s the credit score hit. Every time you apply, lenders do a hard check. Do it twice in a year, and your score drops enough to make future borrowing harder. And if you’ve been relying on a low rate because your income changed, refinancing might not fix the real problem—it just delays it. You’re not solving cash flow issues; you’re just moving them around. People who refinance to pay off credit cards or car loans often end up right back where they started, because they didn’t change their spending habits. The debt didn’t disappear—it just got wrapped into a bigger mortgage.

And here’s the quiet killer: you might not even save money. Some lenders make it look easy, but if you’ve been in your current loan for five years, refinancing might reset your amortization schedule. That means you’re paying mostly interest again for the next few years. You thought you were getting ahead—you’re actually going backward.

There’s no single answer. Sometimes refinancing makes perfect sense—especially if rates have dropped sharply or your credit has improved. But too many people jump in because they saw an ad or a friend did it. The real question isn’t whether you can refinance. It’s whether you should. The posts below break down real cases: who lost money, who got trapped in longer debt, and who actually walked away better off. You’ll see the exact costs, the hidden traps, and the red flags lenders don’t tell you about. This isn’t theory. It’s what happens when people skip the fine print.

What Are the Risks of Remortgaging? Key Dangers You Can't Ignore

Remortgaging can save money-but only if you avoid hidden fees, early repayment charges, and extended loan terms. Learn the real risks of switching mortgages in 2025 and how to protect your finances.

Read More >>