Interest Rate Changes and Remortgage: What You Need to Know

When interest rate changes, fluctuations in the cost of borrowing set by central banks and lenders, they ripple through your mortgage like a wave. If rates go up, your monthly payments could jump—especially if you're on a variable deal. If they drop, you might be sitting on a chance to save thousands by remortgaging, switching your existing mortgage to a new deal with a different lender or rate. It’s not about timing the market perfectly—it’s about knowing when a change in rates makes financial sense for your situation.

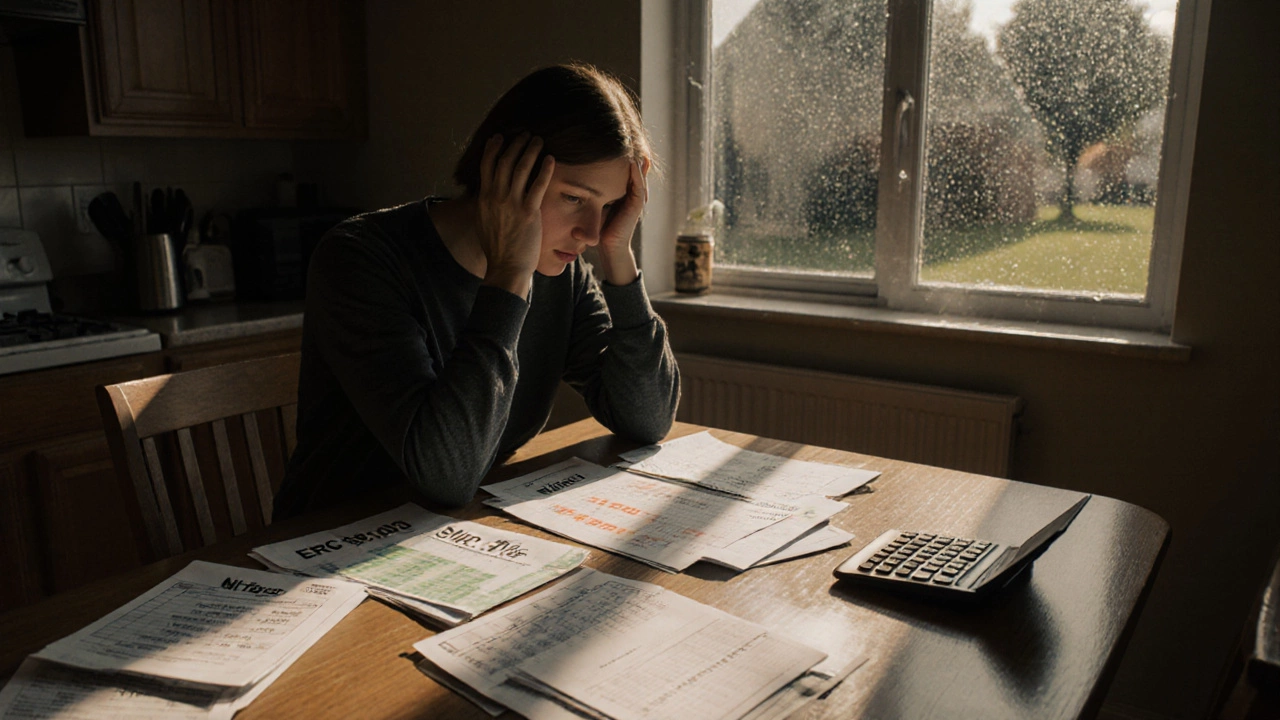

Mortgage rates, the percentage you pay to borrow money for your home, are the engine behind every remortgage decision. When the Bank of England adjusts its base rate, lenders follow suit, often within weeks. That means your current deal might suddenly look expensive compared to new offers. But remortgaging isn’t just about chasing the lowest rate. It’s also about home equity, the portion of your property you truly own, calculated by subtracting your mortgage balance from its current value. If your home has gone up in value, you might be able to unlock cash through remortgaging—even if rates haven’t changed much. Many people use this to pay off high-interest debt, fund home improvements, or cover unexpected costs.

But here’s the catch: remortgaging isn’t free. There are arrangement fees, valuation costs, and sometimes early repayment charges if you’re still in a fixed-term deal. That’s why you need to run the numbers. A 0.5% drop in rate might sound small, but on a £250,000 mortgage, it could save you over £100 a month. Multiply that by five years? That’s £6,000 in your pocket. On the flip side, if you’re stuck with a high fee and your new rate doesn’t beat your current one after costs, you’re worse off. That’s why people who remortgage successfully don’t just chase headlines—they check their own balance, their home’s current value, and their credit score first.

What you’ll find below are real examples, clear breakdowns, and no-nonsense advice on how interest rate changes actually affect your remortgage choices. From when to lock in a new deal to how to use your equity wisely, these posts cut through the noise. No jargon. No fluff. Just what works for UK homeowners right now.

What Are the Risks of Remortgaging? Key Dangers You Can't Ignore

Remortgaging can save money-but only if you avoid hidden fees, early repayment charges, and extended loan terms. Learn the real risks of switching mortgages in 2025 and how to protect your finances.

Read More >>