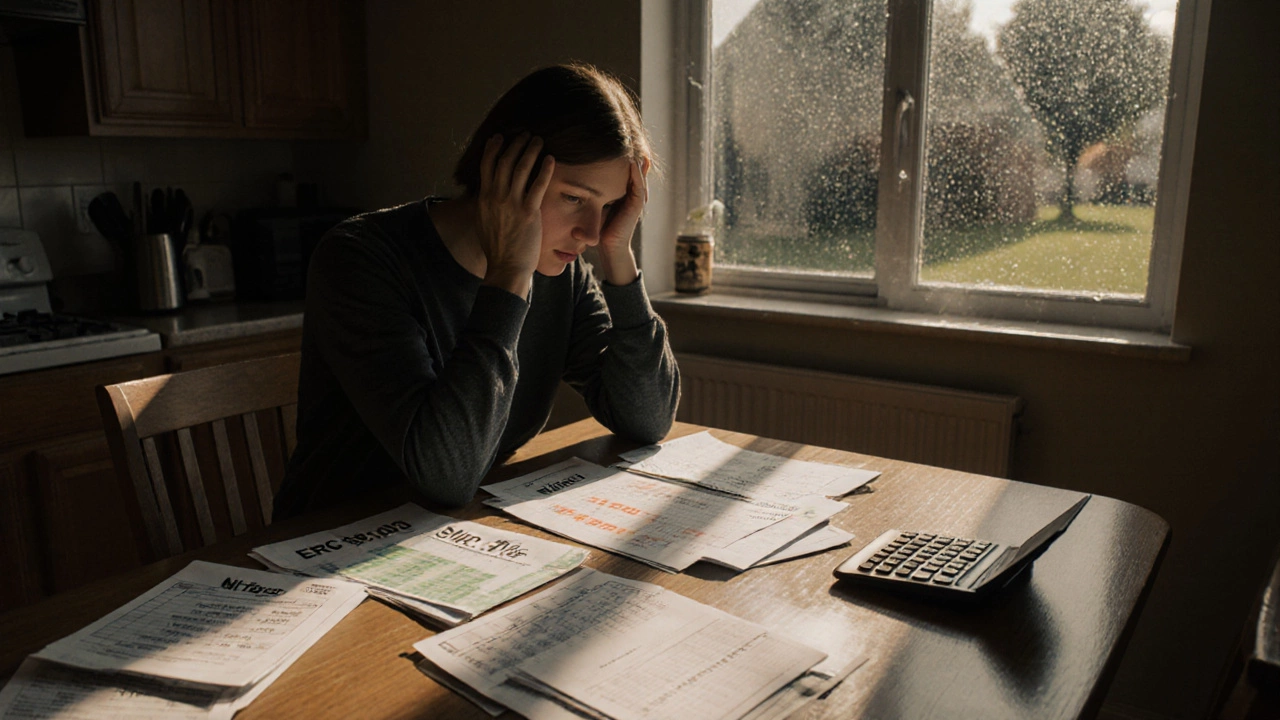

Remortgage Pitfalls: Avoid Costly Mistakes When Refinancing Your Home

When you remortgage, the process of switching your existing mortgage to a new deal, often with a different lender. It’s not just about getting a lower rate—it’s about reshaping your long-term financial path. Many people think remortgaging is a simple way to save money or pull out cash, but the real risks don’t show up in the monthly payment calculator. The equity release, the act of borrowing against the value of your home might sound like free money, but it’s debt with a mortgage attached. And if you don’t understand how it works, you could end up owing more than your home is worth—or worse, lose it.

One of the biggest remortgage pitfalls, common errors people make when refinancing their home loan is ignoring the fees. Arrangement fees, valuation costs, legal charges—they add up fast. Some deals advertise rock-bottom rates, but if you pay £2,000 in fees, you’re not saving anything until year three or four. And if you move again before then? You’re out of pocket. Another trap is extending your loan term. You might drop your monthly payment from £1,200 to £800, but if you go from 15 years left to 30 years new, you’re paying thousands more in interest over time. This isn’t a win—it’s a delay.

Then there’s the home equity loan, a second loan taken out using your home as collateral. People use it for renovations, debt consolidation, or even a holiday. But if your home value drops, or your income changes, that loan becomes a heavy anchor. You’re not just borrowing money—you’re putting your home on the line. And unlike credit cards, you can’t walk away from a mortgage. If you miss payments, the lender can take your house. That’s not a hypothetical risk. It happens every day.

And don’t assume your current lender has your best interests in mind. They’ll often push you to stay with a ‘standard variable rate’ because it’s more profitable for them. But the real savings come from shopping around—even if you’re happy with your current provider. The market changes fast. What looked like a great deal last year might be average now. The best time to check your options? Three to six months before your current deal ends.

There’s also the credit score factor. Every time you apply for a new mortgage, a hard inquiry hits your file. Do it too often, and lenders start seeing you as risky—even if you’ve always paid on time. And if your credit has slipped since you got your original loan, you might not qualify for the rates you expected. That’s why checking your credit report before applying isn’t optional—it’s essential.

What you’ll find below are real examples, clear breakdowns, and honest warnings from people who’ve been through it. Some saved thousands. Others lost thousands. No fluff. No sales pitches. Just what actually happens when you remortgage—and how to make sure you’re not the next cautionary tale.

What Are the Risks of Remortgaging? Key Dangers You Can't Ignore

Remortgaging can save money-but only if you avoid hidden fees, early repayment charges, and extended loan terms. Learn the real risks of switching mortgages in 2025 and how to protect your finances.

Read More >>