If you’ve ever filed a claim after a storm damaged your roof or a pipe burst in the middle of the night, you know how much depends on your home insurance company. But not all insurers treat customers the same. Some respond quickly, pay fairly, and make the process smooth. Others? They drag their feet, deny valid claims, or make it nearly impossible to get a human on the phone.

So which company has the most complaints? The answer isn’t a mystery - it’s tracked every year by state insurance departments and federal agencies. And the data doesn’t lie.

The Data Behind the Complaints

In 2025, the National Association of Insurance Commissioners (NAIC) released its annual complaint index for home insurance. The index compares how many complaints a company receives relative to its market share. A score of 1.0 means the company gets the average number of complaints for its size. Anything above 1.0 means it gets more complaints than expected.

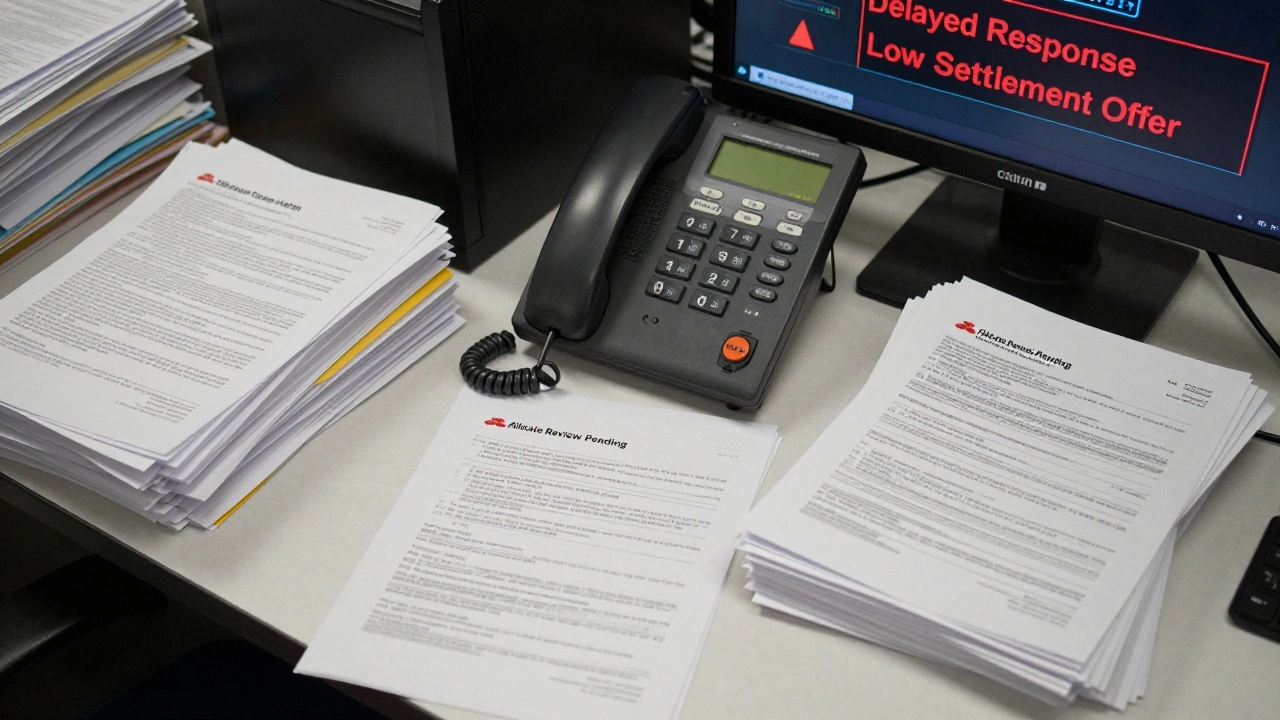

Top of the list? State Farm. Yes, the giant with the green logo and nationwide presence. It had a complaint index of 2.87 - more than double the average. That’s not a fluke. It’s the third year in a row State Farm led the pack in complaints per policyholder.

Why? Because they insure so many people. With over 18 million home policies in the U.S., even a small percentage of unhappy customers adds up. But the real issue isn’t volume - it’s how they handle claims. Customers report long delays, lowball settlement offers, and claims adjusters who seem more focused on saving money than fixing homes.

Who’s Next?

After State Farm, the next highest complaint rates came from:

- Allstate - Index: 2.41

- USAA - Index: 2.19

- Progressive - Index: 2.07

- Travelers - Index: 1.98

USAA is especially interesting. It’s known for serving military families and has a reputation for great service. But even they’re climbing the complaint list. Why? Many policyholders say their claims get stuck in automated systems. One veteran from Texas filed a claim after a tornado destroyed his garage. He waited 11 weeks for an adjuster to show up. When they finally did, they offered $8,000. His contractor’s estimate? $21,000.

Allstate and Progressive follow closely. Both have aggressively expanded into digital-only claims. That sounds efficient - until you’re stuck in a chatbot loop trying to explain why your kitchen ceiling collapsed from a leaky roof.

Who’s Actually Doing Better?

Not all insurers are falling short. Some consistently rank below 1.0 - meaning they get fewer complaints than expected for their size.

- Amica Mutual - Index: 0.53

- Chubb - Index: 0.61

- Auto-Owners - Index: 0.67

- Nationwide - Index: 0.82

Amica, for example, has held the lowest complaint rate for over a decade. How? They don’t outsource adjusters. They hire their own, train them to prioritize customer needs, and empower them to approve claims on the spot. One policyholder in Minnesota had a fire in her basement. Amica sent an adjuster within 24 hours, paid the full replacement cost, and even arranged for temporary housing. No pushback. No delays.

Chubb is another standout. They cater to high-value homes, but their service isn’t just for the wealthy. They offer 24/7 claims support, use in-house contractors, and have a reputation for fair appraisals. One customer in Florida had his $1.2 million coastal home hit by Hurricane Milton. Chubb paid out $1.1 million within 10 days - no fighting over depreciation.

Why Do Complaints Happen?

It’s not just about bad people. It’s about business models.

Big insurers like State Farm and Allstate rely on volume. They make money by selling millions of policies and hoping most people never file claims. When claims do happen, they’re treated as costs to minimize - not obligations to fulfill.

They use software that flags claims as “high risk” based on things like your zip code, past claims history, or even your credit score. Even if your claim is legitimate, the system may auto-reject it or send it to a low-paid adjuster who’s pressured to cut costs.

Smaller, mutual companies like Amica and Auto-Owners operate differently. They’re owned by policyholders, not shareholders. Their goal isn’t to maximize quarterly profits - it’s to keep customers happy so they stay for life. That changes how they handle every claim.

What You Can Do

If you’re shopping for home insurance, don’t just pick the cheapest quote. Look at the complaint data.

Here’s how to check for yourself:

- Go to your state’s insurance department website. Search for “insurance complaint data” or “consumer complaints.”

- Find the NAIC complaint index for 2025. Look for companies with scores above 1.5.

- Read real customer reviews on sites like Consumer Affairs, Trustpilot, and the BBB. Look for patterns: “took 6 months,” “denied water damage,” “couldn’t reach anyone.”

- Ask for references. Call three recent claimants and ask: “Was your claim handled fairly?”

Also, don’t ignore your policy details. A low premium means nothing if your coverage has loopholes. Watch out for:

- Actual cash value (ACV) instead of replacement cost coverage

- Exclusions for mold, sewer backup, or wind damage

- High deductibles - especially for hurricanes or earthquakes

What’s Changing in 2026?

New state laws are starting to crack down. In California and New York, insurers must now respond to claims within 15 days or pay penalties. Florida passed a rule requiring adjusters to be licensed and trained in consumer rights. And the NAIC is pushing for public dashboards that show real-time complaint trends.

Some insurers are responding. State Farm announced in January 2026 that it’s hiring 1,200 new claims specialists and cutting its reliance on third-party adjusters. Time will tell if this is real change - or just PR.

For now, the data is clear: the biggest names aren’t always the best. If you want peace of mind, don’t follow the crowd. Follow the numbers.

Which home insurance company has the most complaints in 2026?

As of 2025 data (the latest available), State Farm had the highest complaint index at 2.87 - more than double the average. Allstate, USAA, and Progressive also ranked high. These companies insure millions, so even small issues add up. Their systems often prioritize cost control over customer service, leading to delays, lowball offers, and denied claims.

Are big insurance companies worse than small ones?

Generally, yes - but not always. Large companies like State Farm and Allstate have more complaints because they serve so many people. But smaller mutual insurers like Amica, Chubb, and Auto-Owners consistently rank lower. Why? They’re owned by policyholders, not shareholders. That means they focus on long-term trust, not short-term profits. Their adjusters aren’t pressured to deny claims, and they often pay faster and more fairly.

How do I find my state’s insurance complaint data?

Visit your state’s Department of Insurance website. Search for “insurance complaint statistics” or “NAIC complaint index.” Most states publish annual reports showing complaint rates per company. You can also use the NAIC’s Consumer Information Source (CIS) tool - it lets you compare insurers side by side by state.

Should I avoid State Farm because of complaints?

Not necessarily - but be cautious. State Farm is still a major player with wide coverage and many agents. If you choose them, make sure you understand your policy inside out. Document everything. Get written estimates from contractors before filing. And be prepared to push back if your claim is undervalued. Many people get fair outcomes - but you’ll need to be proactive.

What should I look for in a home insurance policy to avoid problems?

Avoid policies that only offer actual cash value (ACV) - insist on replacement cost coverage. Make sure your policy includes coverage for sewer backup, mold, and wind damage if you’re in a high-risk area. Check your deductible - especially for named storms. And ask: “Who handles my claim? Is it your employee or a third-party contractor?” If they say “we use contractors,” dig deeper.