Home Insurance Cost Estimator 2026

Property Details

Breakdown

Enter your property details to see how 2026 market factors impact your insurance costs.

Disclaimer: This tool provides an estimate based on general market trends described in the article. Actual premiums will vary by insurer, individual claim history, and specific property characteristics. Always consult with licensed insurance providers for accurate quotes.

Have you opened your latest home insurance quote and felt that familiar knot in your stomach? You are not alone. Across the UK, homeowners are staring at premium hikes that feel less like a standard annual adjustment and more like a shock to the system. If your bill jumped by 15%, 20%, or even double what you paid last year, it is easy to blame greedy insurers. But the reality is far more complex. The sky-high cost of home insurance in 2026 is not just about corporate profit margins; it is a perfect storm of climate change, construction economics, and global financial shifts.

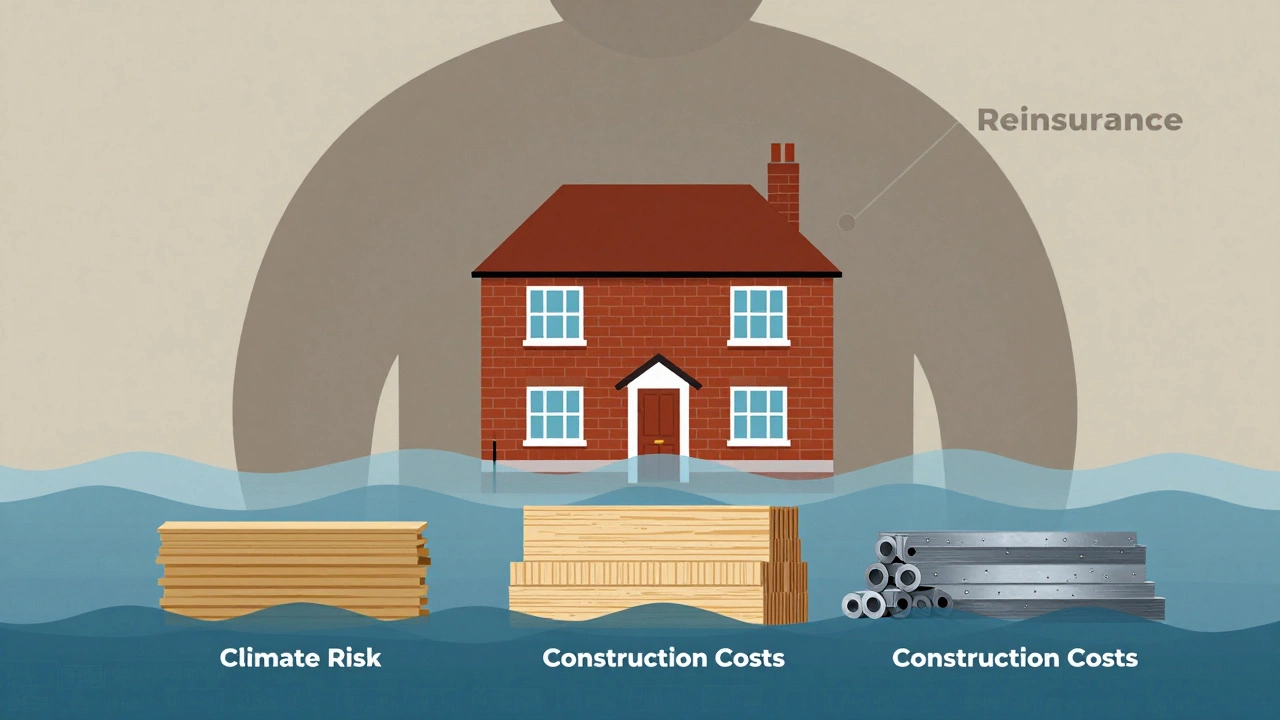

The Climate Change Factor: It’s Not Just Talk Anymore

For years, climate change was a distant concept in policy documents. Today, it is the single biggest driver of insurance costs. Insurers rely on historical data to predict future risks. For decades, they looked back ten or twenty years to calculate how often floods or storms hit specific areas. That model has broken. Weather patterns have shifted so drastically that past data no longer predicts future events accurately.

In 2024 and 2025, we saw unprecedented flooding across southern England and severe wind damage in the north. When an insurer pays out billions in claims for flood damage, they cannot simply absorb those losses. They must raise premiums for everyone in high-risk zones to rebuild their reserves. This is known as "risk pricing." If your home is in a floodplain, even if it hasn't flooded yet, the statistical probability of it happening has increased. Your premium reflects that new reality.

Furthermore, the frequency of "once-in-a-century" storms is increasing. We are now seeing multiple significant weather events within a single year. Each event drains the collective pot of money insurers set aside for payouts. To stay solvent, they charge more upfront. It is a brutal but necessary math equation: higher risk equals higher price.

The Reinsurance Crisis: The Hidden Cost

To understand why your bill is up, you need to look behind the curtain at reinsurance. Reinsurance is essentially insurance for insurance companies. Major providers like Aviva, Admiral, or LV= do not keep all the risk themselves. They buy coverage from massive global firms (like Swiss Re or Munich Re) to protect against catastrophic losses that could wipe them out.

In recent years, these reinsurers have become much more expensive. Why? Because they are also facing record-breaking claims globally-from hurricanes in the US to wildfires in Australia. As global disaster costs rise, reinsurers raise their prices for primary insurers. Those costs are passed directly down to you, the homeowner. In 2023-2024, reinsurance rates for UK properties surged by over 30% in some regions. This hidden layer of cost adds significantly to your final quote.

Construction Costs and Inflation

Insurance isn’t just about paying for stolen TVs; it is primarily about rebuilding your home if it burns down or collapses. The cost of building materials has skyrocketed since the pandemic. Timber, brick, glass, and steel prices remain volatile due to supply chain disruptions and labor shortages.

If your house was built in 1990, its rebuild cost might have been £200,000. Today, replacing that same structure with modern materials and labor could cost £350,000 or more. Insurers adjust your "build cost" sum insured annually to match these inflationary pressures. Even if you haven’t changed anything about your home, the value of what they promise to replace has gone up. Consequently, your premium rises to cover that larger potential payout.

Labor shortages exacerbate this issue. With fewer skilled tradespeople available, builders charge more for their time. This increases the overall cost of reconstruction, which insurers factor into their risk models. You are effectively paying for the inflated cost of carpenters, plumbers, and electricians who might one day fix your roof.

Fraud and Claim Complexity

Another often-overlooked factor is the rise in insurance fraud. According to industry reports, fraudulent claims account for billions in lost revenue annually. From exaggerated water damage reports to staged break-ins, dishonesty drives up costs for honest customers. Insurers spend millions on investigation teams and AI-driven fraud detection software to combat this. These administrative costs are baked into your premium.

Additionally, claims are becoming more complex and expensive to handle. A simple leak today might require extensive mold remediation, structural drying, and health safety inspections-processes that were less rigorous or costly a decade ago. The average cost per claim has risen sharply, forcing insurers to increase baseline premiums to maintain profitability.

| Factor | Impact Level | Explanation |

|---|---|---|

| Climate Events | High | Increased frequency of floods/storms raises risk profiles. |

| Reinsurance Rates | High | Global reinsurers charge more due to worldwide disasters. |

| Build Costs | Medium-High | Inflation in materials and labor increases rebuild values. |

| Fraud | Medium | Higher investigation costs and fraudulent payouts affect pools. |

| Interest Rates | Low-Medium | Insurers earn less on investment reserves, needing more premium income. |

How to Mitigate Rising Costs

While you cannot control the weather or global markets, you can take steps to soften the blow. Here are practical strategies to manage your home insurance expenses in 2026:

- Install Flood Defenses: Many insurers offer discounts for certified flood protection measures, such as airbricks, waterproof doors, or sump pumps. Check with your provider for specific approved products.

- Increase Your Excess: Raising your voluntary excess lowers your monthly premium. Ensure you can afford the higher out-of-pocket cost if you need to make a claim.

- Bundle Policies: Combining home and car insurance with the same provider often unlocks multi-policy discounts that offset individual rate hikes.

- Review Your Contents: Accurately value your belongings. Over-insuring leads to higher premiums for no benefit. Use online valuation tools to get realistic figures for furniture and electronics.

- Shop Around Annually: Loyalty rarely pays off in insurance. Switching providers every year can save you hundreds, as new customer rates are often lower than renewal quotes.

What to Expect in the Future

Will prices drop soon? Unfortunately, most analysts predict stability or further gradual increases. Climate adaptation is a long-term process. Until infrastructure improves and global weather patterns stabilize, insurers will continue to price risk conservatively. However, technology may help. Smart home devices that detect leaks or fires early can reduce claim severity, potentially leading to discounts for tech-enabled homes.

The key takeaway is understanding that your premium is a reflection of real-world economic and environmental pressures. By staying informed and proactive, you can navigate this challenging market without being caught off guard.

Is home insurance getting cheaper in 2026?

No, generally home insurance is not getting cheaper. Due to rising construction costs, frequent severe weather events, and increased reinsurance fees, premiums have continued to rise throughout 2025 and into 2026. Some localized drops may occur for low-risk properties, but the national trend remains upward.

Why did my home insurance go up if I haven't made any claims?

Your premium is based on broader risk factors, not just your personal history. Increases in material costs for rebuilding, regional flood risks, and global reinsurance rates affect all policyholders in similar areas. Even without a claim, the cost for the insurer to cover potential future events has risen.

Can I switch insurers to get a better rate?

Yes, switching is one of the most effective ways to find lower rates. Insurers often offer discounted "new customer" deals. Use comparison websites to check multiple providers annually before your renewal date to ensure you are getting the best market price.

Does living in a flood zone always mean higher insurance?

It usually does, as flood risk is a major cost driver. However, installing government-approved flood defenses can sometimes qualify you for discounts. Additionally, some specialized insurers focus on high-risk areas and may offer competitive rates compared to mainstream providers.

How do interest rates affect my home insurance premium?

Insurers invest the premiums they collect to generate income. When interest rates are high, they earn more on their reserves, which can theoretically allow for lower premiums. However, in 2026, other factors like construction inflation and climate risks outweigh the benefits of higher investment returns, keeping premiums elevated.