Equity Release Compound Interest Calculator

Your Scenario

Results at Age 85

Timing Comparison

Compare debt if taken at age 55 vs current selection:

You’ve spent decades paying off your mortgage. Now, that house is yours-completely debt-free-but your bank account doesn’t quite match your retirement dreams. You hear about equity release, which is a financial product that allows homeowners over 55 to unlock cash from their property without moving out. It sounds like a lifeline. But here’s the real question: when should you actually do it?

There is no single "magic number" for the best age to take equity release. If you trigger it too early, compound interest eats away at your estate faster than you expect. If you wait too long, you might miss out on years of enjoying that extra cash or need it urgently for care costs. The sweet spot usually lands between ages 65 and 70, but your personal situation dictates the exact timing.

The Golden Rule: Wait Until Your Mortgage Is Paid Off

Before you even think about the calendar date, look at your mortgage balance. This is the most critical rule. You should never take equity release while you still have an outstanding repayment mortgage. Why? Because equity release works by releasing the value you *own*. If half your house belongs to the bank via a traditional mortgage, there’s less equity to release, and the rates will be terrible.

If you are 60 years old and still paying a £150,000 mortgage, focus your energy on clearing that debt first. Once that final payment is made, the clock starts ticking on your pure equity. For many people, this happens naturally around age 65 or 66, coinciding with state pension age. This is often the ideal starting point for considering equity release because your major housing liability is gone, and your access to other funds (like private pensions) is open.

Why Age Matters: The Compound Interest Trap

Equity release isn’t free money; it’s a loan secured against your home. With a standard Lifetime Mortgage, which is the most common type of equity release where you keep ownership of your home and borrow against its value, the interest rolls up. This means you don’t pay monthly interest bills. Instead, the interest adds to the loan amount, and then *that* new total attracts more interest.

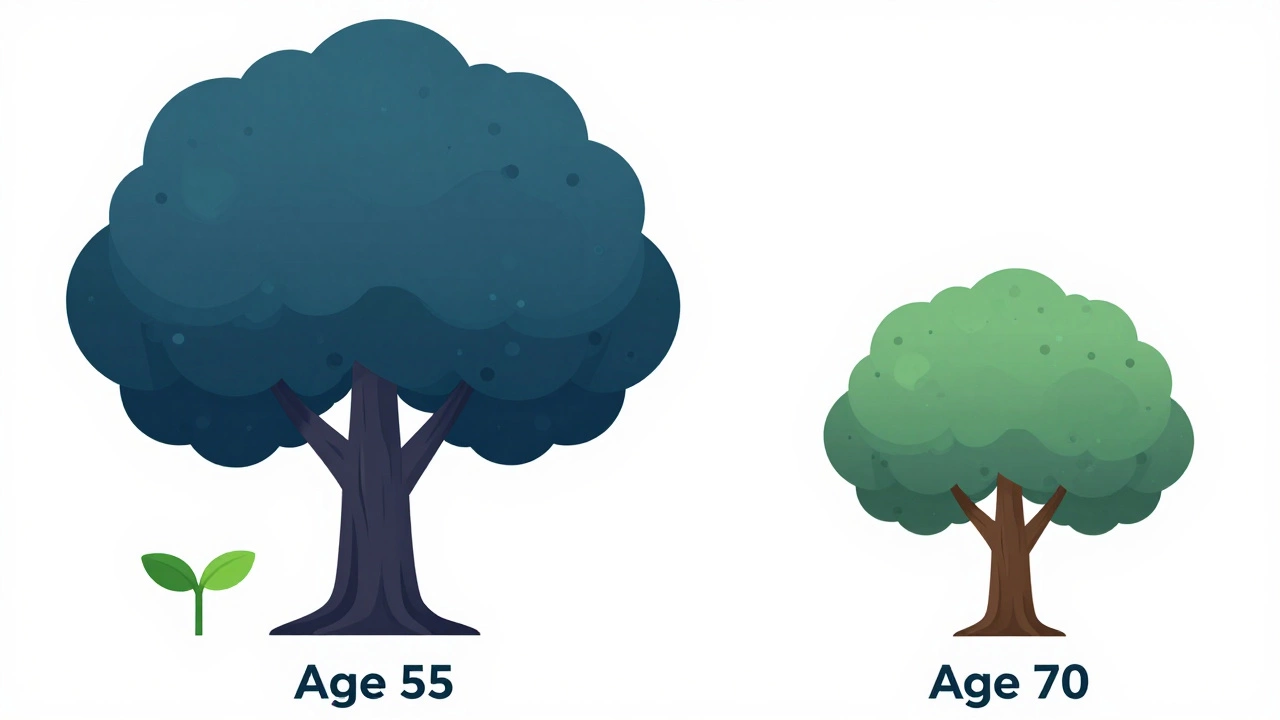

This compounding effect is brutal over time. Let’s look at a realistic scenario. Imagine you take out a £50,000 lifetime mortgage at age 55 with a fixed interest rate of 5% per annum. By the time you are 85, you won’t owe £50,000 plus simple interest. You will owe roughly £134,000. That same loan taken at age 70 would only grow to about £95,000 by age 85. Waiting just 15 years saves you nearly £40,000 in debt.

However, waiting has a cost. That £50,000 could have bought you a new car, paid for holidays, or covered home improvements for those 15 years. The "best" age is the point where the benefit of having the cash outweighs the cost of the future debt.

Common Scenarios: When Earlier Might Be Better

While delaying is mathematically cheaper for your heirs, some life events make earlier action necessary. Here are three situations where taking equity release in your mid-50s or early 60s makes sense:

- Helping Adult Children Buy a Home: Property prices in the UK remain high. If your child is struggling to get onto the ladder, unlocking equity at 55 can provide a deposit gift. Many lenders allow "gift loans" where you use equity release funds to help family members, provided you sign a declaration that the money is a gift, not a loan to them.

- Major Health Issues or Care Costs: If you anticipate needing private nursing care or home adaptations due to health issues, waiting until 70 might mean you’re already frail and unable to enjoy the benefits. Using equity release at 60 to fund care gives you more control and dignity.

- Debt Consolidation: If you have significant credit card debt or personal loans with high interest rates, using lower-interest equity release to clear them can free up monthly cash flow immediately. This is risky and requires strict discipline, but it can stabilize your finances if done carefully.

Lifetime Mortgage vs. Home Reversion: Does Age Change the Choice?

There are two main types of equity release products. Understanding the difference helps you decide if age impacts your choice.

| Feature | Lifetime Mortgage | Home Reversion Plan |

|---|---|---|

| Ownership | You keep 100% ownership | You sell a share of your home |

| Interest | Rolls up over time | No interest, but you lose appreciation on sold share |

| Payout | Lump sum or regular income | Lump sum based on % of current value |

| Best For Age | Flexible, often 55+ | Often better for older borrowers (70+) as valuation risk is lower |

| Estate Impact | Reduces inheritance by loan + interest | Reduces inheritance by percentage of sale price |

Home Reversion Plans, which involve selling a portion of your home to a provider in exchange for a tax-free lump sum or rent-free living rights, are less common now. They tend to favor older applicants because the provider takes on less risk regarding how long they own the asset. If you are younger (55-60), a Lifetime Mortgage is almost always the preferred route because it preserves your ownership stake.

The "Inheritance Protection" Dilemma

A major reason people hesitate to take equity release early is the desire to leave their home to their children. If you take a large lump sum at 55, your estate could be significantly depleted by the time you pass away at 85. However, modern Lifetime Mortgages offer features to mitigate this.

Look for plans with an Inheritance Protection Guarantee. Some providers cap the total debt at a certain percentage of the home’s value (e.g., 75%). This ensures that even if interest rolls up for 30 years, your children will always receive at least 25% of the sale proceeds. Another option is to make voluntary interest payments. Paying the interest annually keeps the loan balance static, preserving more equity for your heirs. This strategy works well if you have enough pension income to cover the interest without dipping into the capital.

Regulatory Safeguards: The Equity Release Council

In the UK, reputable equity release products must be signed up to the Equity Release Council (ERC), which is an industry body that sets standards for equity release products to protect consumers. ERC membership provides crucial protections regardless of your age:

- Negative Equity Guarantee: You will never owe more than the value of your home, even if house prices fall. This applies to both you and your estate.

- Independent Advice: You must receive advice from a qualified adviser who holds the right qualification (usually CII Diploma in Equity Release). This protects you from being sold unsuitable products.

- Right to Remain: You can stay in your home for life, provided it remains your main residence and is maintained in good condition.

Always check that your provider is ERC-accredited. Avoid any company offering "quick cash" schemes that bypass these rules.

How to Decide: A Step-by-Step Checklist

Before signing anything, run through this checklist to determine if now is the right time for you:

- Is my mortgage fully repaid? If no, stop. Focus on paying it off.

- Do I have other assets? Have you exhausted ISAs, savings, and pension drawdown options? Equity release should be a last resort for liquidity, not a first step.

- What is my goal? Are you funding immediate needs (care, home repairs) or long-term enjoyment (travel)? Immediate needs justify earlier action.

- Have I spoken to a family member? While not legally required, discussing the impact on inheritance prevents future conflict.

- Did I get independent advice? Never proceed without a regulated adviser who explains the long-term costs.

- Can I afford the interest? Even if you don’t pay it monthly, understand how much it will grow. Ask your adviser for a projection table showing the debt at age 75, 80, and 85.

Alternatives to Consider First

Equity release is irreversible in most cases. Before committing, consider these alternatives that might achieve similar goals without locking your home:

- Downsizing: Selling your large family home for a smaller flat releases cash upfront and reduces maintenance costs. This is often cleaner than equity release but involves the hassle of moving.

- Reverse Mortgage vs. Secured Loan: If you need a smaller amount of money for a short period, a secured loan against your home might be cheaper than a full equity release plan, though it requires monthly repayments.

- State Benefits Check: Ensure you are claiming all eligible benefits. Sometimes, adjusting your benefit claims can free up cash without touching your asset base.

Frequently Asked Questions

Can I take equity release at age 55?

Yes, most UK providers allow you to start equity release from age 55. However, taking it this early means the interest will roll up for a longer period, potentially significantly reducing the value of your estate. It is generally recommended only if you have an urgent need for funds.

Does equity release affect my council tax or benefits?

Taking a lump sum may affect means-tested benefits like Pension Credit or Council Tax Support because the cash counts as savings. However, if you take the money as a regular income stream, it may be treated differently. Always consult a benefits advisor before applying.

Can I move house after taking equity release?

Yes, you can move, but the new property must meet the provider's criteria (e.g., structural soundness, location). You will likely need to pay a transfer fee, which can range from £500 to £1,500. Some providers allow you to move once, others multiple times.

What happens if house prices drop?

Thanks to the Negative Equity Guarantee offered by ERC members, you will never owe more than the home is worth. If the house sells for less than the loan amount, the lender absorbs the loss. Your heirs will not have to pay the difference.

Is equity release taxable?

The cash you receive from equity release is tax-free. You do not pay Income Tax or Capital Gains Tax on the money. However, if you invest that money and earn interest or dividends, those earnings may be subject to tax.